Points of interest…

- PSLF requires 120 on-time payments while working full-time for a qualifying public service employer.

- A July 2026 court order blocked the new RAP repayment plan, but employer eligibility rules took effect.

- Graduate PLUS loans ended on July 1, 2026, so MSW students must rely on capped federal direct loans.

- Lower-earning social workers often see over $70,000 forgiven because income-driven payments remain affordable.

On July 1, 2026, the elimination of Graduate PLUS loans permanently reshaped how MSW students finance their degrees, while simultaneous updates to PSLF employer rules created a split landscape: one set of tighter standards is in effect, another remains blocked by court order.

Social workers carry an average of $66,000 in student debt, and most already work in settings that qualify for Public Service Loan Forgiveness. That makes the 2026 rule changes both an immediate risk and a planning necessity. For prospective students weighing program costs against long-term debt, MSW scholarships and graduate social work funding guides offer a practical starting point before loans enter the picture.

For new graduates facing the new loan caps, RAP repayment mandates, and uncertainty around what counts as a qualifying employer, the margin for error is now narrower than at any point in the program's history.

How PSLF Works for Social Workers in 2026

Public Service Loan Forgiveness is not a vague promise; it is a precise legal pathway that requires social workers to meet three core conditions simultaneously: eligible employment, eligible loans, and eligible payments.

The 120-Payment Framework

To receive forgiveness, you must complete 120 qualifying monthly payments. A payment counts only when you make it under a qualifying repayment plan while employed full-time by a qualifying employer. Income-driven repayment plans (such as Income-Based Repayment, Pay As You Earn, and Revised Pay As You Earn) typically produce the lowest monthly payments and count toward the 120. The standard 10-year plan also qualifies, but because it pays off the loan in full, there is no balance left to forgive.

Full-time employment is defined by the greater of two standards: 30 hours per week or the employer's own definition of full-time. For example, if your agency considers 35 hours to be full-time, you must work at least 35 hours. Social workers who combine multiple part-time qualifying jobs can meet the threshold if the combined hours total 30 or more per week.

Qualifying Employers for Social Workers

Only employment with certain types of organizations counts toward PSLF. The employer categories most relevant to social workers are:

- Government organizations: any federal, state, local, or tribal government agency. This includes school districts, Child Protective Services, the Department of Veterans Affairs, and public health departments.

- 501(c)(3) nonprofit organizations: hospitals, community mental health centers, family service agencies, and many other nonprofits where social workers are commonly employed.

- Tribal organizations: tribal governments and entities that provide public services.

Employment with private practices, for-profit hospitals, or for-profit mental health companies does not qualify, even if the work serves underserved populations. Some social workers mistakenly believe that working for a nonprofit-affiliated medical group qualifies; always verify the employer's tax status through the PSLF Help Tool or Form 990.

Direct Loans and Consolidation Rules

Only Direct Loans are eligible for PSLF. If you hold older Federal Family Education Loan (FFEL) or Perkins loans, you must consolidate them into a Direct Consolidation Loan. A critical detail: only payments made after the consolidation date count toward the 120. Payments you made on the original loans before consolidation are not credited. This makes early consolidation essential, especially for social workers entering the field with mixed loan types from graduate school.

Parent PLUS loans do not qualify unless consolidated and then repaid under the Income-Contingent Repayment plan, a path that is rarely relevant to MSW graduates but worth noting for those who may have undergraduate PLUS loans.

PSLF Is Not Ending in 2026

A pervasive rumor suggests that PSLF is being phased out or eliminated. In reality, the program is statutory; it was enacted by Congress and cannot be terminated by executive action alone. However, the rules governing PSLF have changed significantly in 2026. Court rulings and administrative adjustments have altered income-driven plan availability, payment counting rules, and even how some employer types are classified. These changes may affect your strategy, but the core forgiveness promise remains intact.

Verifying Eligibility: The PSLF Help Tool and Its Limits

The Department of Education's PSLF Help Tool at StudentAid.gov is the official starting point for checking whether your employer qualifies. The tool cross-references employer tax identification numbers to generate an immediate eligibility determination. However, because rule changes are ongoing, the tool may not fully reflect all 2026 updates. Social workers should also complete and submit the Employment Certification Form annually to create a paper trail and get an official count of qualifying payments. This proactive step prevents surprises when you apply for forgiveness after 10 years of service. For those balancing repayment planning alongside broader financial aid decisions, social work grants for students and practitioners can supplement income-driven strategies during the repayment window.

What Changed on July 1, 2026: Employer Rules, RAP, and Court Orders

On paper, two major PSLF updates were supposed to land on July 1, 2026: a tighter employer eligibility rule and a brand-new income-driven repayment plan called RAP. In practice, federal court rulings have split them apart, one is blocked, the other is live, and social workers need to know which path applies to their loans.

Employer Eligibility Rule Vacated

In October 2025, the Department of Education published a final rule under 34 C.F.R. § 685.219 that would have allowed the Department to disqualify otherwise-qualifying nonprofit employers if a court or administrative body found, by a preponderance of the evidence, that the organization engaged in a "substantial illegal purpose."1 The rule was designed to be prospective only and required the Department to notify borrowers if their employer lost eligibility.1 Before it could take effect, however, a federal court vacated the rule.2 That means the July 1, 2026, effective date never happened. As of today, the older, broader employer eligibility standards remain in place. A social worker employed by a 501(c)(3) or government entity does not need to worry about sudden disqualification and does not need to seek out a new employer solely because of this rule.

Repayment Assistance Plan Takes Effect

Separately, the One Big Beautiful Bill Act authorized the Repayment Assistance Plan, or RAP, which did launch on July 1, 2026.3 RAP is the new default income-driven repayment option for borrowers taking out their first federal student loan on or after that date. It replaces the SAVE plan, which was terminated.3 RAP is fully PSLF-eligible, meaning payments made under RAP count toward the required 120 qualifying payments. The payment formula caps monthly bills at a percentage of discretionary income (the exact percentage and threshold are set by regulation, but the structure mirrors familiar IDR designs), and any remaining balance after 20 or 25 years is forgiven. For PSLF borrowers, tax-free forgiveness arrives after 120 qualifying payments, not a set number of years. Unlike the employer rule, RAP is not blocked by any current court order, and no documented legal challenge is pending as of this writing.3

What Social Workers Need to Do Now

- Existing borrowers in other IDR plans: If you already hold federal loans and are repaying under PAYE, ICR, or another plan, you are not required to switch to RAP. PAYE and ICR remain available through a planned sunset in 2028.3 Continue certifying your income and employment annually, and keep an eye on PSLF qualifying payment counts.

- New MSW graduates or new federal borrowers after July 1, 2026: You will likely be placed in RAP when you enter repayment. Confirm that your employer qualifies (government or 501(c)(3) nonprofit) and submit the PSLF Employment Certification Form early and annually.

- If you hear about employer disqualification: Because the 2025 rule was vacated, any notifications about "substantial illegal purpose" disqualifications are not in effect. Rely on official Federal Student Aid communications, not rumors, to verify your employer's status.

For MSW financial aid and scholarships, understanding these shifts is just one piece of the puzzle. For most social workers already on the PSLF track, the July 1, 2026, changes amount to a quiet non-event. The employer eligibility rule never materialized, and the new repayment plan only touches new borrowers. The critical task remains the same: work for a qualifying employer, stay in an IDR plan, and document every year of service.

Questions to Ask Yourself

Employer Eligibility Risk Check for Common Social Work Settings

The newest PSLF rule forces a practical trade-off for social workers: your passion for a community-based mission must now be weighed against the risk that your employer could one day be deemed ineligible, pausing your forgiveness clock. Starting July 1, 2026, the Department of Education can disqualify nonprofits and government agencies that engage in a "substantial illegal purpose," even if their 501(c)(3) status remains intact.1 The rule is narrow in scope, with officials expecting fewer than ten employers nationwide to be affected annually,2 but because it targets conduct rather than broad categories, many social work settings deserve a closer look.

How the July 2026 Rule Redefines Employer Eligibility

The final regulation introduces a conduct-based exclusion: if an employer is found, by a preponderance of the evidence, to have a substantial illegal purpose, it can lose PSLF eligibility.3 The rule explicitly mentions civil rights violations, unlawful gender-affirming care, and illegal immigration assistance as examples.4 Notably, there is no revenue test, lobbying threshold, or automatic exclusion for entire sectors. Most community mental health centers, child welfare agencies, and hospital social work departments will remain fully qualifying employers unless they are directly implicated in the targeted activities.

Crucially, the rule protects borrowers: any PSLF credit earned before a disqualification date is permanently retained.1 Social workers can continue to earn forgiveness progress at other eligible employers after a job change. Employers can also regain eligibility by implementing a corrective action plan or by demonstrating that ten years have passed since the disqualifying conduct occurred.3

Which Social Work Settings Face the Most Uncertainty?

- Community mental health centers and child welfare agencies: These are generally low-risk. Most operate as straightforward 501(c)(3) nonprofits or government entities and are not the focus of the new exclusions. However, a center that actively facilitates unlawful immigration assistance as a core service could come under scrutiny.4

- Hospital social work departments: Typically safe, whether in public, nonprofit, or government-owned hospitals. The exclusion targets the employer entity, not an individual department. If the hospital system itself violates the rule, all employees, including social workers, would be affected.3

- Advocacy nonprofits: These carry higher risk. Organizations that engage in lobbying, litigation, or direct advocacy around civil rights, immigration, or gender-affirming care may be more likely to intersect with the targeted legal areas.4 The qualitative nature of the "substantial illegal purpose" test means that even a well-intentioned advocacy group could be challenged, especially given ongoing legal disputes over the rule's statutory authority.2

How to Verify Your Employer's Status Before You Rely on PSLF

Social workers should take three concrete steps. First, confirm the employer's 501(c)(3) designation or government status using the IRS Tax Exempt Organization Search tool. Second, review the organization's most recent IRS Form 990, which details its mission, programs, and any significant legal or regulatory actions. While the form will not explicitly state PSLF eligibility, it can reveal red flags like ongoing civil rights litigation or unusual revenue sources tied to the targeted conduct. Third, use the updated PSLF Help Tool at StudentAid.gov to generate an official employer eligibility determination. The tool now reflects the new rule and can flag employers under review or already disqualified. Retain a copy of the determination each year.5

The Staffing Firm Trap: Why Your Worksite Isn't Your Employer for PSLF

For contract social workers placed at government agencies or nonprofits through a staffing firm, the employer of record is the staffing agency, not the worksite. If the staffing firm is a for-profit company, its employees are not eligible for PSLF, even if they work full-time at a qualifying government office. To qualify, the social worker must be directly employed by the eligible employer. If you are in a contract role, check your W-2: the name on that form is your employer for PSLF purposes. Some staffing firms have set up separate nonprofit subsidiaries to employ contract workers for this exact reason, but that structure is rare. Social workers who handle immigration social work cases should be especially careful, as their employer's legal exposure in that area could directly affect PSLF status under the new rule.

New Loan Caps and the End of Grad PLUS: What MSW Students Need to Know

What are the new federal loan limits for MSW students in 2026, and how does the elimination of Grad PLUS loans affect financing? Starting July 1, 2026, the One Big Beautiful Bill Act (OBBBA) eliminated the Graduate PLUS loan program for most graduate students and imposed new annual and aggregate caps on federal borrowing.1 For social work students, these changes reshape how an MSW is funded.

The New Federal Borrowing Limits for MSW Students

Under OBBBA, MSW programs are classified as non-professional graduate degrees.3 This means social work students can borrow up to $20,500 per year in federal Direct Unsubsidized Loans, with a graduate aggregate limit of $100,000.1 Across all degrees, the lifetime federal loan cap is $257,500, but for a standard two-year MSW, the total federal loan availability from the program itself is capped at $41,000.4 These numbers replace the previous system where Grad PLUS loans could fill the gap between standard loan limits and the full cost of attendance. For context, graduate professional students (such as those in law or medicine) face a higher annual cap of $50,000 and an aggregate limit of $200,000 under the same legislation.1

What This Means for Higher-Cost MSW Programs

Many MSW programs, especially at private universities or out-of-state public institutions, charge annual tuition and fees well above $20,500. Without Grad PLUS, students attending these programs must cover the shortfall through other means. Options include private student loans, institutional aid, scholarships, graduate assistantships, and employer tuition assistance.4 Some schools may expand their own aid packages in response, but relying on private loans increases long-term repayment risk. Choosing a lower-cost program, such as an in-state public university or an accredited online MSW with competitive tuition, becomes an even stronger financial strategy. MSW scholarships and grants can also close funding gaps that federal loans no longer cover. The elimination of Grad PLUS fundamentally shifts the cost-benefit analysis for prospective students, encouraging a focus on total debt minimization.

Rumors of Expanding Forgiveness: The Reddit Post

A recent Reddit post on r/socialwork claimed that "29 programs now qualify for the $200k professional" loan forgiveness program.5 While this post was user-generated and not an official announcement, it has sparked interest in whether forgiveness pathways are broadening. The $200,000 figure may refer to expanded Public Service Loan Forgiveness or a new targeted program, but no verified details are available. For social workers pursuing PSLF, the core rules remain: work for a qualifying employer, make 120 qualifying payments under an income-driven plan. Students should not base borrowing decisions on unverified social media claims and instead consult the Department of Education for current, official information.

Grandfathering Rules: Current vs. Future MSW Students

If you began your MSW program before July 1, 2026, and have already taken out federal loans under the old rules, you may be grandfathered for up to three years.2 This legacy exception allows eligible students to continue accessing Grad PLUS loans under prior terms until 2029. Incoming cohorts starting in fall 2026 or later will immediately face the new caps and cannot rely on Grad PLUS. Current students should contact their financial aid office to confirm their status and plan for any gap in funding if they are near the new limits. The grandfathering window provides a temporary bridge, but eventual transition to the new system is inevitable for all graduate borrowers.

Related Articles

PSLF Vs. NHSC Vs. State Forgiveness: Which Path Maximizes Relief for Social Workers?

Choosing between Public Service Loan Forgiveness (PSLF) and a targeted loan repayment program is not an either-or decision. It is a sequencing puzzle. The right strategy can multiply forgiveness, especially for social workers carrying six-figure debt. Here is how the major options compare, which ones stack, and how to time your applications.

Federal vs. State vs. NHSC: A Side-by-Side Look

PSLF cancels your remaining federal student loan balance tax-free after 120 qualifying payments while you work for a qualifying nonprofit or government employer. It is broad but requires a decade of service. The NHSC Loan Repayment Program zeroes in on clinical social workers: licensed LCSWs who commit to two years in a Health Professional Shortage Area receive $50,000.1 State programs fill the gaps with higher awards, often tied to similar or longer commitments. Minnesota offers $40,000 over two years for LICSWs.2 Michigan provides up to $300,000 over two years for clinical social workers with a master's degree.2 North Carolina awards $150,000 over three years for eligible behavioral health providers.2 New York's Licensed Social Worker Loan Forgiveness Program pays $26,000 over four years and requires state residency.2

Stacking Rules and the Double-Count Strategy

Most state programs and the NHSC explicitly stack with PSLF.3 That means you can receive a state or NHSC award and still make qualifying PSLF payments during your service commitment. NHSC and state awards are typically paid as a lump sum or periodic installments directly to your loan servicer. They reduce your principal but do not replace your monthly income-driven payments. Because your PSLF-qualifying payment is calculated from your income, not your balance, you can reduce your overall debt while accumulating PSLF months simultaneously. North Carolina's program requires a case-by-case check of stacking rules, so confirm with the program administrator.2 The optimal sequence: apply for NHSC or a state grant early in your career, satisfy the program's service term, then continue toward PSLF if a remaining balance exists. This way, you slash your balance first and have the remainder forgiven after 120 total payments. social work grants for practitioners can supplement this approach at any stage.

Which Programs Are Currently Funded?

As of 2026, the NHSC LRP opens applications annually through HRSA and remains well-funded.1 Minnesota's Social Worker Loan Forgiveness is active but competitive.2 New York's program is currently accepting applications.2 Michigan's program, while generous, may have limited funding cycles subject to state budget allocations.2 North Carolina's program is subject to periodic appropriations; check for open application windows before preparing your materials.2 Because slots are limited, gather your documentation early and apply as soon as the cycle opens.

What Social Workers Actually Earn: National Salary Snapshot

Income-driven repayment plans tie monthly payments directly to your adjusted gross income, so your earnings shape both your monthly outlay and the total amount forgiven after 120 qualifying payments. The table below shows national wage estimates for social worker occupations, highlighting the variation across specializations from child and family practice to healthcare settings. These percentiles provide a realistic baseline for estimating your own repayment trajectory under PSLF.

| Occupation | Mean Annual Wage | 25th Percentile | Median | 75th Percentile |

|---|---|---|---|---|

| Social Workers | $67,050 | $48,680 | $61,330 | $78,500 |

| Child, Family, and School Social Workers | $62,920 | $47,480 | $58,570 | $74,060 |

| Healthcare Social Workers | $72,030 | $55,360 | $68,090 | $83,410 |

| Social Workers, All Other | $74,680 | $52,010 | $69,480 | $95,390 |

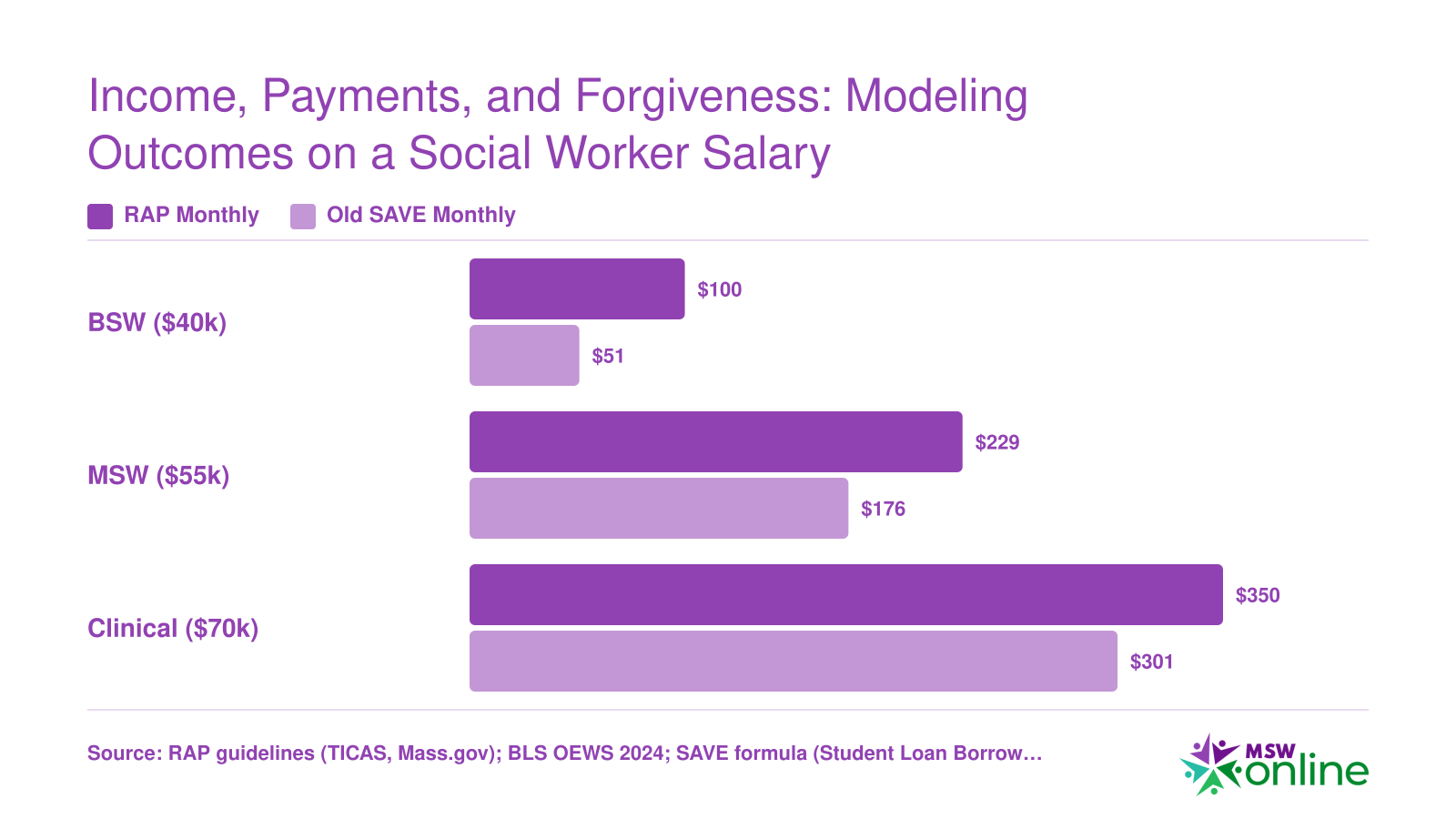

Income, Payments, and Forgiveness: Modeling Outcomes on a Social Worker Salary

This illustration compares monthly payments under the new Repayment Assistance Plan (RAP) and the now-unavailable SAVE plan for three social worker income levels, assuming $70,000 in federal student loans. After 120 qualifying payments, any remaining balance is forgiven tax-free at the federal level (state tax treatment varies). With RAP, a $40,000 earner pays $12,000 total and has $58,000 forgiven; a $70,000 earner pays $42,000 total and sees $28,000 forgiven. Under the former SAVE formula, monthly payments would have been lower, resulting in greater forgiveness but a now-inaccessible path.

Social workers with modest salaries often receive the largest forgiven balances under PSLF. Because income-driven payments stay low, less principal is repaid over 10 years, meaning more debt is wiped out at the end. This makes the program a powerful career-long financial tool for the profession.

Step-By-Step PSLF Strategy for Social Workers: Before, During, and After 120 Payments

As of July 1, 2026, structural changes to PSLF have redefined which social work employers qualify and which repayment plans lead to forgiveness, making a step-by-step strategy essential. Many social workers discover too late that missing one form or misjudging an employer's eligibility can add years to their debt. Here's how to navigate the process from start to finish.

Before You Start Making Qualifying Payments

- Create your FSA ID at StudentAid.gov and use it to review your loan portfolio. Only Direct Loans qualify, so consolidate any FFEL or Perkins loans into a Direct Consolidation Loan.

- Choose the right income-driven repayment (IDR) plan. For new borrowers in 2026, the Repayment Assistance Plan (RAP) often yields the lowest payments. If you borrowed earlier and are grandfathered into SAVE or IBR, confirm those plans still count for PSLF under current court rulings; check the Federal Student Aid website for the latest guidance.

- Submit your first Employer Certification Form (ECF) as soon as you start an eligible job. Do not wait. Even if you are not yet in repayment, this locks in your employer's eligibility and establishes a record. Use the PSLF Help Tool to generate the form, and have your HR office sign it.

While You Work Toward 120 Payments

- Recertify your income every year. IDR plans require annual income documentation, and missing the deadline can cause your loans to revert to a standard plan, where payments may not count.

- Submit an ECF annually or whenever you change jobs. The government does not track qualifying employment automatically; you must prove it. Keep copies of every ECF, pay stub, and employment contract.

- Monitor your qualifying payment count on StudentAid.gov. After each ECF is processed, your count updates. If you see a discrepancy, contact your servicer immediately. Do not assume it will self-correct.

After You Reach 120 Payments

- Submit the PSLF application (not an ECF) once you believe you have 120 qualifying payments. Expect a processing timeline of 60 to 90 days. Keep making payments if you are uncertain about your count; any overpayments will be refunded.

- If payments are miscounted, request a manual review and cite the IDR account adjustment, a one-time revision that corrected many past counting errors. Social workers who previously held ineligible employment may still get some months counted if they consolidated before the adjustment deadline.

The Single Biggest Mistake Social Workers Make

Avoid the trap of waiting until year 10 to submit your first ECF. Many social workers discover at that point that their employer was never qualifying because the organization's tax status or contract structure failed the new 2026 employer eligibility rules. Annual ECF submissions let you catch ineligibility early, switch employers if needed, and build an audit-proof record of your service. This kind of deliberate record-keeping mirrors the discipline that MSW field placement tips reinforce from the earliest stages of training. Treat your PSLF paperwork as you would clinical documentation: timely, organized, and never left to chance.

Alternative Paths: Part-Time, Contract, and Private-Practice Social Workers

Not every social worker holds a traditional full-time job with a single qualifying employer, but PSLF still offers pathways for those with part-time schedules, contract positions, or private-practice aspirations.

Part-Time Workers: Combining Hours for PSLF Credit

Part-time social workers at qualifying government or nonprofit organizations can earn PSLF credit as long as they meet the full-time threshold of at least 30 hours per week. For many, that means combining two part-time qualifying positions. The hours from both jobs are added together, and each employer must certify your employment. Submit a separate Employment Certification Form for each employer, and make sure the combined hours consistently reach 30 or more. This approach is especially common for MSWs who split their time between a school district and a community health clinic, or between a hospital and a government agency.

Contract and 1099 Workers: The Employer-of-Record Problem

Social workers hired as independent contractors (1099) face a fundamental PSLF barrier: the employer of record is not the worksite but the staffing agency or consulting firm that issues the paycheck. Because these intermediaries are typically for-profit entities, even if you perform services inside a qualifying hospital or school, your payments will not count toward PSLF. The solution is to pursue direct-hire positions where the government or nonprofit that benefits from your work is also your legal employer. If you currently contract with a staffing agency, ask the organization you serve whether it can bring you on as a W-2 employee. Some social workers negotiate a transition from contractor to employee status precisely to regain PSLF eligibility.

Private Practice: PSLF Is Off the Table, but Alternatives Exist

If you own a private therapy or consulting practice, you are ineligible for PSLF under current rules because the entity is for-profit, no matter how many underserved clients you serve. However, several alternative relief options remain:

- IDR forgiveness: Under income-driven repayment plans, any remaining balance is forgiven after 20 or 25 years of qualifying payments. This forgiveness is currently federally taxable, but it does not require public-service employment.

- State loan repayment programs: Many states offer their own forgiveness or repayment assistance programs for mental health professionals willing to work in underserved areas or for designated employers. These often do not mandate government or nonprofit status, so they can apply to private-practice clinicians. loan forgiveness for rural social workers is one well-documented avenue worth exploring if your caseload includes underserved rural populations.

- Refinancing: If you earn a strong income and are willing to give up federal protections, refinancing with a private lender can slash your interest rate and accelerate debt payoff. This removes PSLF eligibility permanently, so it is best reserved for those committed to private practice long-term.

Keeping a Foot in the Door: The Hybrid Strategy

Some social workers maintain a part-time qualifying public-service job while building a private practice on the side. This lets you earn PSLF credit during the years it takes to reach 120 payments, while still growing your own client base. balancing work and an MSW program requires similar discipline, and the same time-management principles apply here: calendar your hours, communicate with supervisors, and track your certification paperwork carefully. Once your loans are forgiven, you can transition to full-time private practice. The hybrid approach requires careful planning and employer approval, but it gives you the financial safety net of PSLF without sacrificing your long-term career goals.

The average Master of Social Work graduate carries $66,000 in student loan debt. For many social workers, Public Service Loan Forgiveness can erase that balance after ten years of qualifying payments. This makes PSLF a cornerstone of financial planning for the profession.

Common Questions About PSLF for Social Workers

Understanding the latest Public Service Loan Forgiveness rules is critical for social workers planning their financial future. Below are answers to the most pressing questions about PSLF eligibility, payment strategies, and recent program changes as of 2026.