Points of interest…

- Social workers earning a median of $61,330 must plan aggressively because moderate salaries leave a narrow savings margin.

- Public Service Loan Forgiveness can free thousands of dollars that would otherwise divert from retirement contributions.

- At 77, social worker Cheryl Alexander still works two jobs, illustrating how high living costs extend careers well past traditional retirement age.

- Closing a clinical practice triggers specific ethical and legal obligations for client record retention and licensure.

How do social workers actually retire given moderate salaries and heavy student debt? The median social worker earns $61,330, according to the Bureau of Labor Statistics, a figure that leaves little room for aggressive saving after loan payments and housing costs. The profession's focus on others often means financial self-care gets postponed.

That tension plays out in real time for Cheryl Alexander, a 77-year-old social worker and family counselor in San Diego 1profiled by Marketplace.org. She still works two jobs, including a tour company she has run for 30 years, because the high cost of coastal living makes retirement a two-job proposition.

The result is a retirement landscape where conventional benchmarks rarely hold. Social workers must build plans around public service loan forgiveness, 403(b) matches, and late-career income streams that look nothing like the single-employer pension model. Understanding MSW career change options later in a career can open supplemental paths worth building into that plan.

How Much Do Social Workers Need to Retire Comfortably?

The central tension in retirement planning for social workers is this: the profession demands years of graduate education and often carries significant debt, yet the salaries it produces leave a narrower margin for saving than many comparable careers. Knowing your actual target number is the first step toward closing that gap.

Start With the 80% Rule

Financial planners commonly suggest replacing 80% of your pre-retirement income to maintain your standard of living once you stop working. Applied to social workers, the math is straightforward. The median annual wage for social workers across all specializations is approximately $61,330, according to Bureau of Labor Statistics data. Eighty percent of that figure puts your annual retirement income target at roughly $49,000.

Healthcare social workers earn more on average, with a median closer to $68,090, making their 80% target around $54,500 per year. Child, family, and school social workers cluster around a $58,570 median, landing at about $46,860. The specialty you chose shapes the target significantly.

Translate That Into a Total Savings Goal

Once you have an annual income target, the multiply-by-25 rule converts it into a total nest egg figure. The rule is based on the 4% withdrawal rate, meaning you can draw 4% annually from a portfolio without depleting it over a 30-year retirement. Multiply your annual target by 25 and you get the savings you need on day one of retirement.

- Median social worker ($61,330 income): Annual target of ~$49,000. Savings goal: approximately $1.225 million.

- Child/family/school social worker ($58,570 income): Annual target of ~$46,860. Savings goal: approximately $1.17 million.

- Healthcare social worker ($68,090 income): Annual target of ~$54,500. Savings goal: approximately $1.36 million.

Those figures can feel daunting. They are meant to be clarifying, not discouraging.

The Spread Matters

Social workers do not all earn at the median. The 25th percentile for the broader social worker category sits at $48,680 annually, while the 75th percentile reaches $78,500. A social worker earning near the lower end faces a savings target under $1 million but has less disposable income to get there. One earning near the upper end has more room to save but a larger number to hit.

The profession also compresses the accumulation window. Many social workers carry graduate school debt into their late 20s or early 30s, delaying meaningful contributions to retirement accounts by five to ten years. That delay is not insurmountable, but it does require deliberate catch-up strategies later in the career.

Location Changes Everything

A social worker earning $61,000 in rural social work salary vs urban contexts illustrates a stark contrast: the same income in rural Mississippi and in San Diego produces very different financial realities. Regional cost of living shifts both what you can save and what you will need in retirement. The state salary breakdown later in this article maps out those differences so you can calibrate your target to where you actually live and plan to retire.

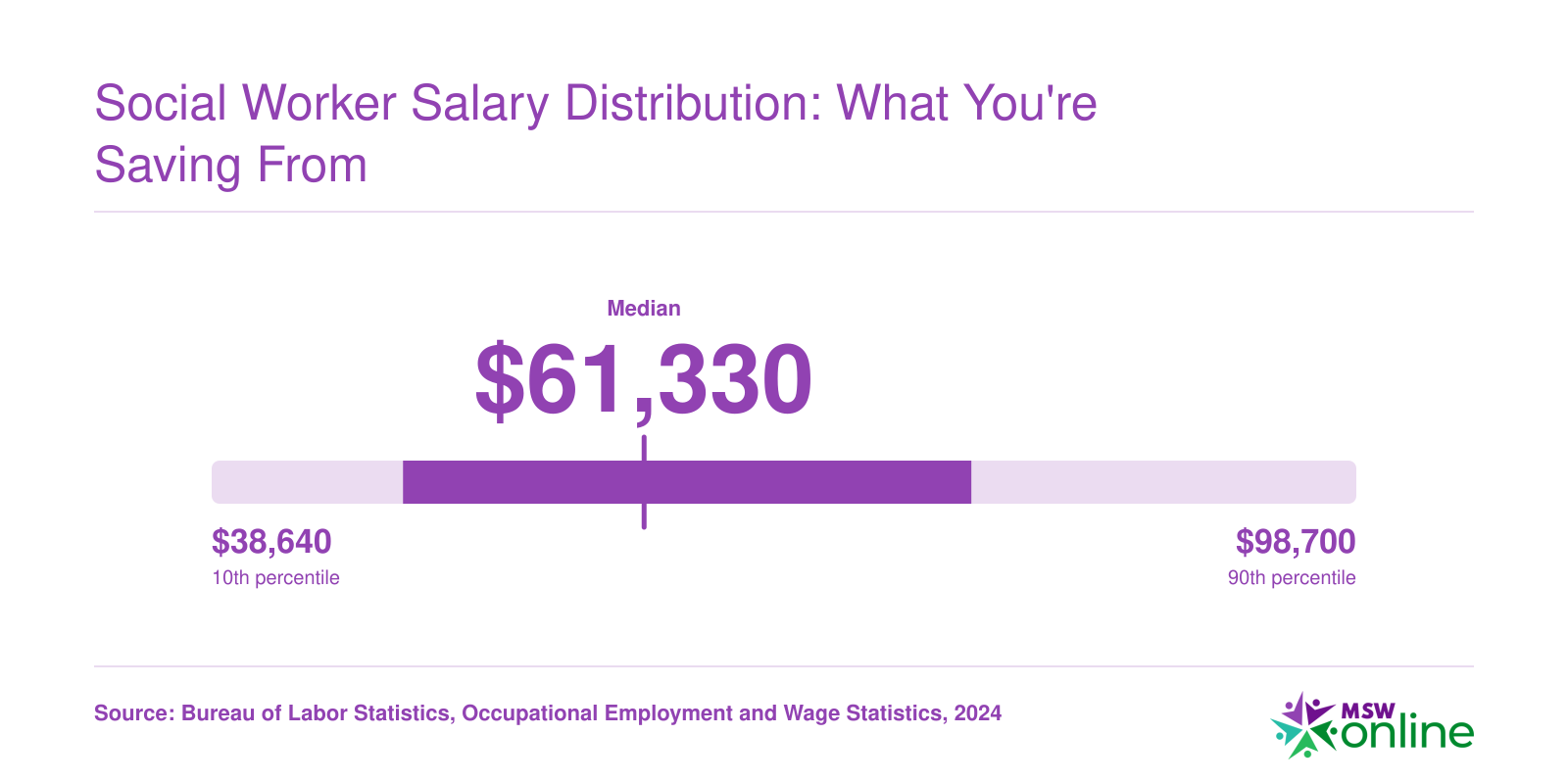

Social Worker Salary Distribution: What You're Saving From

Most social workers earn between roughly $49,000 and $79,000 a year, with a national median of $61,330 according to Bureau of Labor Statistics data. That moderate salary range shapes every retirement calculation, from how aggressively you can contribute to a 403(b) to how long your savings will need to last. Understanding where you fall in this distribution is the first step in building a realistic retirement plan.

Retirement Plans Available to Social Workers: 403(B), Pensions, and IRAs

The retirement accounts available to you hinge on where you work. Social workers in nonprofit settings, schools, hospitals, and government agencies typically access 403(b) plans or defined-benefit pension systems. Those in private practice or employed by for-profit firms encounter 401(k) plans instead. Every social worker also has access to individual retirement accounts (IRAs), which serve as essential supplements when employer-sponsored plans offer limited matching or when you want to diversify your tax treatment.

403(b) Plans: The Nonprofit Backbone

Most social workers employed by charitable institutions, community mental health centers, schools, and hospitals participate in 403(b) defined-contribution plans. In 2026, you may defer up to $24,500 of salary into a 403(b), with an additional $8,000 catch-up contribution if you are age 50 or older.1 If you are between ages 60 and 63, SECURE 2.0 legislation permits a "super catch-up" of $11,250 instead of the standard $8,000, allowing you to accelerate savings in the years immediately preceding retirement. Social workers with 15 or more years of service at the same qualifying employer may also be eligible for an additional $3,000 annual catch-up, capped at $15,000 over a career.3 Because contribution limits and catch-up provisions change annually, check current IRS retirement plan limits for the most current figures before setting your payroll elections.

Employer matches vary widely across nonprofits. Some agencies contribute 3 to 5 percent of salary, while others offer nothing. Vesting schedules, which dictate when employer contributions become fully yours, range from immediate to six-year graded vesting.2 Consult your employer's benefits office or plan administrator for the specific vesting table and match formula documented in your 403(b) summary plan description.

Government Pensions and Hybrid Systems

Social workers in state, county, and municipal agencies often participate in defined-benefit pension plans rather than or in addition to 403(b) accounts. These pensions calculate retirement income as a percentage of your final average salary multiplied by years of service. Vesting typically occurs after five to ten years, though some jurisdictions require as few as three. The Bureau of Labor Statistics Occupational Outlook Handbook for social workers and your employer's human resources website or union contract will detail your system's vesting schedule, benefit formula, and any cost-of-living adjustment provisions.

Individual Retirement Accounts (IRAs)

Traditional and Roth IRAs allow social workers to save beyond employer plans. For 2026, the contribution cap is $7,500, plus a $1,100 catch-up contribution if you are 50 or older.1 Traditional IRA contributions may be tax-deductible, subject to income limits if you are covered by an employer plan; qualified withdrawals in retirement are taxed as ordinary income. Roth IRA contributions are made with after-tax dollars, but qualified distributions are entirely tax-free. Roth eligibility phases out at modified adjusted gross incomes of $153,000 to $168,000 for single filers and $242,000 to $252,000 for married couples filing jointly in 2026.2 Visit IRS.gov to confirm current phase-out ranges and deductibility thresholds before opening or funding an IRA.

Questions to Ask Yourself

Coordinating Social Security, Pensions, and Savings on a Social Worker's Salary

Most social workers reach mid-career with retirement income spread across two or three separate buckets, and the balance between those buckets varies enormously depending on whether you work for a government agency or a nonprofit.

The Three-Legged Stool, and Why One Leg Is Often Missing

The classic retirement framework imagines three sources of income: Social Security, an employer pension or plan, and personal savings. For government-employed social workers, all three legs may be present. For the large share of social workers employed by nonprofits and community organizations, the employer pension leg is simply gone. There is no defined-benefit plan. What replaces it, if anything, is a 403(b) that depends entirely on how much you chose to contribute and whether your employer offered any match.

According to Bureau of Labor Statistics data, social worker salaries in 2026 span a wide range. At the 25th percentile, social workers earn roughly $44,000 per year. At the 75th percentile, that figure climbs to around $70,000. Those anchor points matter when you start modeling what retirement actually looks like.

Two Realistic Scenarios

Consider a county child protective services worker earning $68,000 near the 75th percentile. After 25 years, she may retire with a defined-benefit pension paying 50 to 60 percent of final salary, combined with a Social Security benefit she has been accruing throughout her career. Her three legs are intact, though the pension may reduce her Social Security benefit if the government pension offset rules apply in her state.

Now consider a clinical social worker at a nonprofit counseling center earning $46,000, near the 25th percentile. Her employer offers a 403(b) with a partial match but no pension. Over 30 years of saving, with consistent contributions and reasonable market returns, she may accumulate a meaningful nest egg, but she is carrying far more investment risk and contribution responsibility than her government counterpart.

The Social Security Claiming Tradeoff

Claiming Social Security at 62 reduces your monthly benefit by roughly 25 to 30 percent compared to waiting until full retirement age (67 for most current workers). At 70, the benefit is about 24 percent higher than at 67. On a lower lifetime salary, that gap compounds. A social worker who earned $46,000 on average might receive around $1,400 per month at 62, versus closer to $1,900 at 67, and over $2,300 at 70. Waiting even a few years, if health and savings allow it, has an outsized effect at lower income levels.

A Simple Priority Waterfall

If you are actively building retirement savings, the sequence matters more than the account label:

- Employer match first: Contribute at least enough to capture any employer match in your 403(b) or 401(k). That is an immediate 50 to 100 percent return on that slice of money.

- Roth IRA next: If your income qualifies, max out a Roth IRA before adding more to your workplace plan. Tax-free growth is especially valuable if your salary is modest now but you expect steady income in retirement.

- Then max out the 403(b) or 401(k): The 2026 contribution limit is $23,500 for most workers, with a $7,500 catch-up for those 50 and older.

- Taxable brokerage last: Only open a taxable investment account once the tax-advantaged options above are fully funded. For most social workers, that threshold takes years to reach.

Coordinating these streams is not complicated in principle, but it does require knowing exactly what your employer plan offers, what your projected Social Security benefit looks like, and whether any pension or government offset rules apply in your state.

Public Service Loan Forgiveness and Its Impact on Retirement Savings

For social workers carrying MSW debt, Public Service Loan Forgiveness (PSLF) is one of the most powerful retirement planning tools you have, even though it looks like a loan program on the surface. Every dollar forgiven is a dollar you can redirect toward retirement accounts in your 40s and 50s, the exact window when compounding does its heaviest lifting.

How PSLF Works for Social Workers

The rules are straightforward, even if the paperwork is not. You need 120 qualifying monthly payments1 (10 years' worth) made under an income-driven repayment (IDR) plan or the 10-year Standard plan, while working full-time for a qualifying employer. Qualifying employers include federal, state, local, and tribal government agencies plus 501(c)(3) nonprofits1, which covers most community mental health centers, hospitals, schools, and social service agencies where MSWs practice. Only Direct Loans qualify; older FFEL or Perkins loans must be consolidated first.

As of January 2026, roughly 1.22 million borrowers have been approved for PSLF2, with about $90.6 billion forgiven2 and an average of $74,300 wiped out per borrower.3 Another 2.6 million borrowers have certified qualifying employment and are working toward the finish line.3 The program is functioning far better than it did before the 2021-2022 limited waiver and the 2022-2024 IDR account adjustment, which together fixed decades of tracking errors.

The Retirement Math

Here is the opportunity cost to take seriously. If you spend a decade making modest IDR payments instead of maxing a 403(b), you give up compounding on those contributions. But once your balance is forgiven, redirecting what was a $400 to $600 monthly loan payment into a 403(b) or IRA, especially after age 50 when catch-up contributions kick in, can close much of that gap by traditional retirement age. Forgiven amounts under PSLF are also federally tax-free, so there is no surprise tax bill to derail the plan. MSW financial aid and scholarships can further reduce the debt load you bring into repayment in the first place.

Pitfalls That Cost People Years

- Wrong repayment plan: Payments on the graduated or extended plans do not count. Stick with IBR, PAYE, ICR, or the 10-year Standard.4

- Employment certification gaps: Submit the PSLF form annually and every time you change employers. Do not wait until year 10 to reconstruct history.

- Consolidation missteps: Consolidating after some qualifying payments used to reset your count. Rules have shifted, so confirm before you consolidate.

- 2026 rule changes: A new federal rule effective July 1, 2026, was partially blocked in mid-20265, and PAYE and ICR closed to new borrowers on that date.4 If you are already enrolled, verify your plan status directly with your servicer rather than relying on secondhand information.

Related Articles

Social Worker Salaries by State: Planning Around Regional Cost of Living

Your salary shapes how much you can save, but your cost of living determines how far that savings stretches in retirement. The table below draws from the Bureau of Labor Statistics Occupational Employment and Wage Statistics (2024) and covers median annual wages and employment totals across selected states for three major social work categories. Notice that the highest paying states, such as California, the District of Columbia, and New Jersey, are also among the most expensive places to live. A healthcare social worker earning a $92,970 median in California faces steep housing, tax, and daily expenses that can sharply reduce actual retirement contributions. Meanwhile, a social worker in a lower cost state like Mississippi or Alabama may earn less on paper but could accumulate a comparable nest egg because everyday expenses consume a smaller share of take home pay.

| State | Social Work Specialty | Median Annual Wage | Total Employment |

|---|---|---|---|

| California | Healthcare Social Workers | $92,970 | 19,680 |

| District of Columbia | Healthcare Social Workers | $92,600 | 490 |

| Washington | Social Workers, All Other | $96,550 | 870 |

| Massachusetts | Social Workers, All Other | $94,000 | 590 |

| Georgia | Social Workers, All Other | $92,750 | 1,180 |

| South Carolina | Social Workers, All Other | $91,940 | 500 |

| Mississippi | Social Workers, All Other | $89,860 | 280 |

| Texas | Social Workers, All Other | $89,520 | 2,700 |

| Alabama | Social Workers, All Other | $89,170 | 450 |

| Oregon | Healthcare Social Workers | $85,150 | 2,050 |

| Connecticut | Healthcare Social Workers | $81,900 | 2,010 |

| New Jersey | Healthcare Social Workers | $81,710 | 4,390 |

| Connecticut | Child, Family, and School Social Workers | $78,940 | 5,360 |

| District of Columbia | Child, Family, and School Social Workers | $78,920 | 2,800 |

| New Jersey | Child, Family, and School Social Workers | $78,150 | 6,410 |

| Washington | Healthcare Social Workers | $75,670 | 4,970 |

| Minnesota | Healthcare Social Workers | $72,330 | 2,530 |

| California | Child, Family, and School Social Workers | $69,250 | 55,220 |

| Massachusetts | Child, Family, and School Social Workers | $67,880 | 9,830 |

| Hawaii | Child, Family, and School Social Workers | $66,450 | 1,080 |

| New York | Child, Family, and School Social Workers | $65,430 | 27,220 |

| Minnesota | Child, Family, and School Social Workers | $65,010 | 6,430 |

| Colorado | Child, Family, and School Social Workers | $63,560 | 7,840 |

At 77, San Diego social worker and family counselor Cheryl Alexander still works two jobs. Alongside her counseling practice, she runs Italian Excursion, a one woman tour company she has operated for 30 years, guiding small groups through the Italian countryside twice annually. Her reason for continuing to work is straightforward: the high cost of living near the beach makes full retirement unrealistic. Her story, profiled by Marketplace.org, illustrates a reality many social workers face.

Second Careers and Income Streams for Retiring Social Workers

Retiring from social work rarely means retiring from work entirely. For many MSWs and clinical social workers, the real tension is not whether to keep working but how to structure that work so it supplements income without recreating the burnout that prompted retirement in the first place.

A Real-World Model: Skills That Travel

Cheryl Alexander, a San Diego family counselor 1featured in a July 2026 Marketplace.org piece, offers a striking example of what this can look like. At 77, she runs Italian Excursion, a one-woman tour company she has operated for 30 years, leading small groups through the Italian countryside twice a year. The high cost of living near the beach in San Diego means she continues working two jobs in retirement. What makes her story instructive is not the specifics of her business but the logic behind it: the communication skills, cultural competence, group facilitation, and empathy that define social work translate cleanly into guiding strangers through unfamiliar territory, literally and figuratively.

Social workers spend careers assessing needs, managing group dynamics, and holding space for people in transition. Those are not profession-specific skills. They are marketable ones.2

Seven Concrete Paths Worth Considering

- Agency consulting: Nonprofits and government agencies regularly hire experienced practitioners on contract to review programs, train staff, or support accreditation processes.

- Part-time private practice: Maintaining a clinical license opens the door to seeing a reduced caseload on your own schedule, often at rates well above salaried employment.2

- Mediation and conflict resolution: Social workers with family or community practice experience are well-positioned for certified mediator roles in divorce, workplace, or community disputes.

- Life coaching: While distinct from therapy, coaching draws on assessment and motivational interviewing skills and can be built into a largely remote practice.

- Adjunct faculty: MSW programs at community colleges and universities frequently hire experienced clinicians to teach practice courses, often per course or per semester.

- Nonprofit board service: Some boards compensate members, particularly for committee chair roles or organizations with governance stipends.

- Freelance training and workshop facilitation: Agencies, schools, and healthcare systems pay for workshops on topics like trauma-informed care, de-escalation, and cultural humility.

Why Even Modest Income Changes the Math

Generating $15,000 to $20,000 annually from part-time or freelance work in retirement is not a luxury buffer. It is a meaningful structural shift. That income reduces what you need to withdraw from savings each year, which extends how long a portfolio lasts and reduces sequence-of-returns risk in the early years of retirement. For social workers who entered the field with student debt and spent careers in nonprofit or government salaries, the median annual wage for counseling and social work roles ranges from roughly $43,000 to $61,0003, leaving a thinner margin for error in retirement savings than peers in higher-earning professions. A supplemental income stream does not fix a savings gap, but it buys time and flexibility. Exploring the full range of career opportunities in social work can help you identify which skills translate most directly into viable income streams.

Keep Your License or Close It: The Decision That Shapes Your Options

The highest-paying second-career options, private practice and consulting, depend on holding an active clinical license. A social worker who lets a license lapse to avoid continuing education costs loses access to those income streams. Before making that decision, it is worth calculating the actual annual cost of maintaining licensure against the potential hourly rate from even occasional clinical work. In many states, the math favors keeping the license active well into semi-retirement. The next section covers what closing a practice actually requires if and when that decision does make sense.

Closing a Practice: Client Records, Licensure, and Ethical Obligations

What do social workers need to do with client records when they retire?

Retiring from clinical practice is not simply a matter of locking the office door. The NASW Code of Ethics and every state licensing board impose concrete obligations that follow you beyond your last session. Treating these as optional is a mistake: violations can result in disciplinary action even after you have stopped practicing, and in some cases expose you to civil liability. Understanding social workers' ethical responsibilities to clients in this context is essential before you finalize any retirement timeline.

Client Record Retention: The Numbers Vary More Than You Think

Most states set a minimum retention period of six to seven years from the date of last service for adult clients. California, Texas, Florida, Connecticut, and Colorado all require seven years for adult records.1 New York and Virginia require six years.2 Minor clients are a different matter entirely, and the variation is significant:

- California and Florida: records for minors must be kept until the client turns 18, plus three additional years.1

- Texas: the rule is five years after the minor turns 18, or seven years from the last service date, whichever is longer.3

- New York: records must be retained until the client turns 22.2

- Connecticut: retention extends until the client turns 21.4

- Virginia: minor records must be kept for 18 years from the date of last service.5

If you billed Medicare or Medicaid, a separate federal requirement extends retention to ten years.6 NASW goes further than any state, strongly recommending that practitioners retain records indefinitely when possible.7 Given that former clients may resurface years later, or that records may be subpoenaed in legal proceedings, that recommendation is worth taking seriously.

One rule applies everywhere: you cannot destroy records at the moment of practice closure.7

The Practice Closure Checklist

A responsible wind-down requires planning that typically begins 60 to 90 days before your last day. Texas licensing rules, for example, specify a 90-day notice window.3 The core steps include:

- Notifying active clients in writing with enough lead time to find new providers.

- Offering referrals and, where appropriate, facilitating warm handoffs to other clinicians.

- Obtaining written consent before transferring records to a new provider.

- Designating a records custodian, a person or entity responsible for maintaining files after you close. A business associate agreement is required if that custodian will handle electronic records under HIPAA.3

- Securing paper records in a locked, access-controlled location and encrypting any digital files.

- Notifying insurance panels so you are removed from active provider directories.

- Informing your state licensing board of your closure or change in practice status.

HIPAA does not expire when your practice does. Unsecured electronic records held post-retirement remain your legal responsibility, and a breach carries the same penalties it would have during active practice.

Licensure Surrender vs. Inactive Status

When you stop practicing, you have two options: surrender your license entirely or convert it to inactive status. Surrendering is permanent, and reinstating a lapsed license can require retaking exams and completing continuing education from scratch. Inactive status, by contrast, typically involves a reduced renewal fee and no continuing education requirement, but it preserves your credential.

If there is any chance you will consult, supervise, or provide part-time therapy after retirement, keeping your license in inactive status is the more practical choice. Many social workers who transition into second careers in coaching, consulting, or organizational roles find that a valid license, even an inactive one, adds credibility and reopens clinical options if circumstances change.

A Retirement Planning Checklist for Social Workers

Use this checklist to move from vague intentions to concrete retirement readiness. Each item addresses a different piece of the planning puzzle, tackle them in order or prioritize the ones you have been putting off.

- Calculate your income-replacement targetDetermine the percentage of your current salary you will need in retirement, most planners suggest 70–80 percent. Factor in healthcare costs, which are typically higher for retirees than working professionals, and any debt you expect to carry past your last paycheck.

- Verify your pension or retirement-plan vesting statusContact your employer's HR or benefits office to confirm whether you are fully vested in your pension or 403(b) employer match. If you are close to a vesting cliff, it may be worth staying long enough to lock in those funds.

- Apply for Public Service Loan Forgiveness certificationIf you have federal student loans and work for a qualifying nonprofit or government employer, submit an Employment Certification Form now, do not wait until you hit 120 qualifying payments. Eliminating student debt before retirement frees up savings capacity.

- Review client record retention obligationsCheck your state licensing board's requirements for how long clinical records must be maintained after closing a practice. Plan for secure storage or transfer well in advance of your last day to stay in compliance with legal and ethical standards.

- Explore licensing requirements for a second careerIf you are considering a post-retirement income stream, consulting, teaching, tour guiding, or private practice in a new state, research the credentials, business licenses, or continuing-education hours you will need before you make the leap.

- Maximize catch-up contributionsWorkers age 50 and older can contribute extra to 403(b) and IRA accounts each year. If your budget allows, increase your contributions to the maximum permitted. Even a few years of catch-up contributions can meaningfully close a savings gap.

- Evaluate relocation for cost-of-living savingsCompare your current housing and living expenses against lower-cost regions where you could maintain your quality of life. A move can stretch a modest retirement portfolio significantly further, especially for social workers retiring from high-cost metro areas.

- Consult a fee-only financial plannerA fee-only advisor has no incentive to sell you products. Schedule at least one comprehensive session to stress-test your retirement plan, coordinate Social Security timing, and identify gaps while you still have earning years ahead of you.

Frequently Asked Questions About Retirement for Social Workers

Retirement planning raises practical questions that social workers at every career stage need to think through. The answers below draw on the financial strategies, regulatory considerations, and career transition options covered throughout this guide.