Points of interest…

- By 2028, MSW programs must show graduates out-earn typical bachelor's holders or lose federal loans.

- New caps limit graduate borrowing to $50,000 per year and $200,000 lifetime, eliminating Grad PLUS.

- Social workers can still stack PSLF with NHSC loan repayment and state programs.

- Median social work earnings fall below the bachelor's-degree threshold, threatening program funding and workforce supply.

How do you borrow for an MSW when the government is tightening the rules on graduate lending? A July 5, 2026 op-ed in The Tuscaloosa News by Lydia Seabol Avant framed the stakes: new federal policies, including the loss of Grad PLUS loans and a 2028 earnings-test rule, could strip federal aid from programs where graduates earn less than the typical bachelor's degree holder.1 Social work, alongside teaching and journalism, is squarely in the crosshairs.

MSW graduates routinely carry six-figure debt into salaries that often fall below that earnings threshold. College costs have climbed 107 percent over two decades, already stretching student budgets thin. For incoming MSW students in 2026, the math has shifted in ways that demand careful, immediate scrutiny.

What Changed: 2026 Federal Student Loan Policy Overview

For MSW students, the latest overhaul of federal student loan policy sets up an immediate squeeze between the true cost of a graduate degree and how much the government will now lend. While the stated goal is to stem runaway borrowing, the new rules tighten the spigot at the very moment social work programs are producing practitioners for mental health, child welfare, and community services , fields where salaries rarely track the debt taken on.

The End of Graduate PLUS Loans for New Borrowers

As of July 1, 2026, the Graduate PLUS Loan program is no longer available to students who have not received a Direct Loan disbursement for their current degree program before that date.1 This means anyone starting an MSW in fall 2026 or later cannot use Grad PLUS to cover costs beyond the standard Direct Unsubsidized Loan limits. Students already enrolled and who had a Direct Loan disbursed by June 30, 2026, are considered legacy borrowers: they may continue borrowing under the old rules for up to three academic years or the remainder of their program, whichever is shorter, provided they maintain continuous enrollment.1 A leave of absence longer than 180 days breaks that eligibility. Existing loans are not affected, but the pipeline for new social work graduate students has been permanently altered.

New Annual and Aggregate Borrowing Caps

With Grad PLUS off the table, graduate students now face tighter Direct Unsubsidized Loan caps. For professional-degree programs, a category that includes the MSW, the new annual maximum is $50,000 and the aggregate (lifetime) cap is $200,000.1 These limits took effect on the same July 1, 2026, timeline. The federal student loan lifetime limit is $257,500 (excluding Parent PLUS Loans), but the $200,000 aggregate cap for graduate-only borrowing effectively walls off the upper tier for anyone who did not already accrue undergraduate debt.1 For many MSW students pursuing financial aid and scholarships, especially those at private or out-of-state institutions where total program costs can easily top $100,000, the math no longer works without substantial personal savings, institutional aid, or private loans.

The 2028 Earnings-Test Rule: A Looming Threat

A second, quieter shift arrives in 2028: a new federal rule will require graduate programs to demonstrate that their alumni earn more than the typical bachelor's degree holder. Programs that fail this earnings test in two out of three years lose access to federal Direct Loans and could eventually lose Pell Grant eligibility.2 As columnist Lydia Seabol Avant noted in a July 2026 column in The Tuscaloosa News, this provision directly endangers careers that are essential but historically underpaid, including social work. If MSW programs cannot clear the bachelor's-degree earnings threshold, future students may be unable to secure any federal loans for those degrees, regardless of the societal need for the services they provide.

Why the Impact Is Amplified for Social Work

The policy changes arrive against a backdrop of steeply rising college costs: a U.S. News & World Report analysis cited in the same Tuscaloosa News piece pegs the two-decade increase at 107%.2 For social work, where median salaries often hover in the $50,000, $60,000 range, the borrowing caps mean that fully financing an MSW through federal aid is no longer a given, even at public universities. The 2028 earnings benchmark threatens to shutter or radically reshape the very programs that train the workforce for vulnerable communities. The combined effect is a tightening vice: less upfront aid, and a future rule that could cut off aid entirely if graduate earnings do not climb fast enough.

How Graduate PLUS Elimination and New Borrowing Caps Affect MSW Students

For the 2025-2026 academic year, the average annual tuition for an online MSW program is $9,810, with a range from $7,125 to $11,774. While these figures appear manageable, the total cost of attendance including fees, books, and living expenses often pushes graduate costs far higher. Under the new federal policy, MSW students face a dramatically altered borrowing landscape that may force many to seek private loans with fewer protections.

The End of Graduate PLUS Loans

Graduate PLUS loans have long served as the safety net for MSW students, covering any gap between other financial aid and the full cost of attendance. Their elimination means that borrowing is now capped, leaving students to rely solely on Direct Unsubsidized Loans. For graduate students, the annual limit on Direct Unsubsidized Loans has historically been $20,500, but the new policy introduces an increased cap of $50,000 per year for some programs, while Graduate PLUS loans are phased out entirely. Without the PLUS option, students in higher-cost programs will need to find alternative funding.

How the $50K Annual Cap Creates a Funding Gap

The $50,000 annual cap may sound generous, but it must cover tuition, fees, and living expenses. Using 2025-2026 data, online MSW tuition averages $9,810, but on-campus costs vary widely. In-state public programs range from $7,214 to $12,606, well within the cap. However, out-of-state public programs cost $16,929 to $35,346, and private nonprofit MSW programs average $28,017.3 When adding books, supplies, and room and board, total costs can exceed $50,000, especially at private universities in high-cost cities. Students at these programs face immediate shortfalls.

Online vs. On-Campus Costs Under the New Caps

Online MSW programs offer a more affordable path, with per-credit costs like $711.16 at University at Buffalo4 and $1,099 at Rutgers University,5 keeping total tuition well below the cap. On-campus students, particularly out-of-state and private school attendees, are more vulnerable. A student at a private institution with $28,000 tuition plus $20,000 in living expenses would exceed the cap by several thousand dollars annually. This gap hits hardest for those who cannot relocate for in-state residency and for whom online programs may not offer the clinical placements they need.

The Private Loan Trap for Social Workers

To cover the shortfall, many MSW students will turn to private loans. However, private loans lack income-driven repayment plans and do not qualify for Public Service Loan Forgiveness, the cornerstone of debt relief for social workers. Interest rates are typically higher and variable, creating a far riskier debt profile for graduates entering a field where starting salaries often hover around $50,000 to $60,000. This mismatch could deter talented candidates from pursuing necessary clinical training. Proactively pursuing MSW scholarships and assistantships can reduce dependence on any loan type.

Timeline: Current Students vs. Future Applicants

The new caps apply to students enrolling in or after fall 2027, as the full policy framework takes effect in 2028. Those already in an MSW program should confirm with their financial aid office whether they are grandfathered under existing Graduate PLUS rules. Students applying for fall 2027 and beyond must plan for capped federal borrowing and may need to aggressively seek social work grants and state loan repayment programs to fill the gap without resorting to private debt.

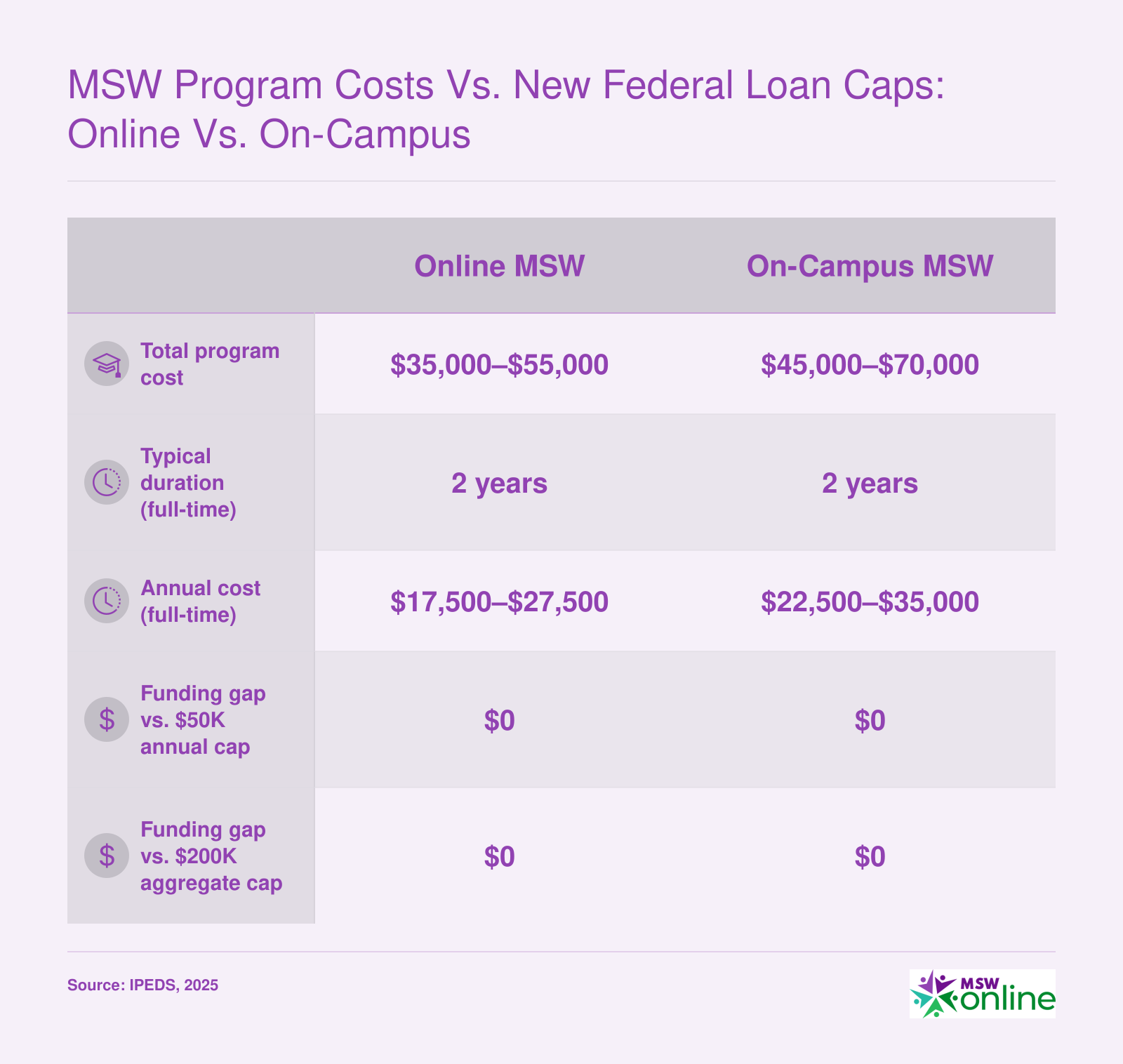

MSW Program Costs Vs. New Federal Loan Caps: Online Vs. On-Campus

The new graduate borrowing caps of $50,000 per year and $200,000 aggregate apply to all federal loans. MSW programs, both online and on-campus, typically cost well below these limits, so students are unlikely to hit the caps solely from their degree.

The 2028 Earnings-Test Rule: Why MSW Programs Could Lose Federal Loan Access

The 2028 earnings-test rule places federal student loans for Master of Social Work programs at immediate risk because social work earnings often fall below the threshold set for advanced-degree professions. Beginning in 2028, the U.S. Department of Education will strip federal Direct Loan eligibility from graduate programs whose completers fail to out-earn typical bachelor's degree holders in two out of three consecutive years.1 For a field where median pay hovers near or below that benchmark, the practical result is clear: many MSW programs are on a collision course with funding cuts that would shrink the pipeline of licensed social workers at a moment when mental health demand is surging.

How the Earnings Test Works for Graduate Programs

The rule establishes a straightforward comparison: a graduate program's completers (graduates from a specific award year) must show earnings that exceed the median earnings of working adults ages 25-34 who hold only a bachelor's degree.1 The benchmark data comes from the U.S. Census Bureau2 and is applied to a four-year earnings lookback window. Programs with fewer than 30 completers in a cohort are exempt from the test, but most MSW programs easily surpass that threshold.

The evaluation timeline is already underway. Reporting starts October 1, 2026.1 The first formal earnings calculation arrives in early 2027, based on the 2021 completer cohort. A second calculation follows in early 2028, and if a program fails both , or any two out of three consecutive award years , the earliest possible loss of Direct Loan eligibility is July 1, 2028.1 Once lost, Title IV aid termination lasts at least three years.

Why MSW Salaries Are a Vulnerable Target

National labor data underscores the problem. Social workers earned a median annual wage of $61,330, with the broader "Counselors, Social Workers, and Other Community and Social Service Specialists" group at just $57,480. Child, family, and school social workers , the largest single category , earned $58,570, while healthcare social workers reached $68,090. By comparison, the typical bachelor's-degree holder in the benchmark age group often clears $62,000. The overlap is dangerous. Any MSW program whose alumni cluster in lower-paying roles risks missing the earnings premium entirely in a given year.

This is not a hypothetical. When program-level earnings data lag behind even bachelor's-level averages, the two-of-three failure threshold becomes a nearly automatic trigger. Since the lookback period spans four years of earnings, a single weak cohort can haunt a program through multiple evaluation cycles. Small wage improvements or shifts in graduate career paths may not register quickly enough to prevent loan access loss.

No Public Service Exemption Exists

The final rule contains no blanket carve-out for public service fields.1 Social work, teaching, and other mission-driven professions are subject to the same earnings premium test as any other graduate program. While advocates argued that underfunded but essential careers should be shielded, the Department of Education's published framework confirms that MSW programs must meet the same standard.3 There is no alternative pathway that factors in the societal value of the work or the chronic underpayment baked into social services.

The Parachute Option and Its Limits

Programs that fail the test do have a limited stopgap. Under a "parachute" provision, an estimated 600 affected programs nationwide could freeze new enrollment for two years while attempting to boost graduate outcomes.4 If they still fail after that, full loan eligibility termination follows. Even this temporary fix carries enrollment cliffs and reputational damage that could deter prospective students. For smaller social work departments, a multi-year freeze often means program closure.

Consequences for the Social Worker Pipeline

Losing federal Direct Loans does more than raise student costs: it cuts access to Grad PLUS and income-driven repayment plans that make MSW degrees financially viable. Fewer enrollments mean fewer licensed clinical social workers at a time when the Bureau of Labor Statistics projects faster-than-average demand for mental health and substance use treatment roles. Rural social work communities, where salaries are lowest, could face the worst enrollment drops, widening an already persistent care gap.

The timeline leaves little room for inaction. Programs that see early warning signs in the 2027 calculation will have roughly a year to adjust before the 2028 cutoff. For current and incoming MSW students, the rule turns program-level earnings data from a post-graduation curiosity into an urgent pre-enrollment screening tool. MSW financial aid and scholarships are worth researching now, before program eligibility begins to narrow.

Questions to Ask Yourself

PSLF Employer Eligibility Changes for Social Workers in 2026

The 2026 PSLF Rule That Wasn't

Social workers tracking Public Service Loan Forgiveness updates may have seen headlines about major employer eligibility changes set for July 1, 2026. The U.S. Department of Education finalized a rule that would have excluded employers engaged in a "substantial illegal purpose" from PSLF qualifying employment.1 However, a federal court vacated the rule just hours before its effective date, meaning the proposed exclusions never took effect.2 The core categories of qualifying employers remain unchanged: U.S. federal, state, local, or tribal government organizations, and 501(c)(3) nonprofit organizations.

While the vacatur means no immediate disruption, the attempted policy shift signals a long-term push to narrow PSLF's scope. Social workers should understand which employer types are safe, which have always been ineligible, and how to protect their certification path.

Social Work Employer Types and PSLF Eligibility

Most social workers will find their employers fit squarely within traditional qualifying categories.3 The following employer types continue to be PSLF-eligible after July 1, 2026:

- State and county agencies: Child protective services, public health departments, and adult protective services all qualify as government employers.

- Community mental health centers: Nearly always structured as 501(c)(3) nonprofits, these remain fully eligible.

- Hospitals: Nonprofit and public hospitals qualify. For-profit hospitals do not.

- Public schools: School districts are government entities, so school social workers qualify regardless of whether the district is a direct employer or an intermediate unit.

- 501(c)(3) nonprofits: Applies to many social service agencies, family support organizations, and advocacy groups.

School Social Workers: Still Covered

School social workers employed by public school districts remain eligible for PSLF. The vacated rule did not target educational institutions, and public schools are government employers under the program's statutory definition. This includes charter schools that operate as public schools. Social workers in private, nonprofit schools may also qualify if the school holds 501(c)(3) status. Only for-profit private schools are ineligible, which is a small segment of the K-12 market.

Employers That Signal Caution

Social workers should exercise extra diligence if employed by:

- For-profit behavioral health companies: Even if they hold government contracts to provide community-based services, for-profit entities do not qualify for PSLF, and this has been the case since the program's inception. The vacated rule would not have changed this.

- For-profit contractors staffing public agencies: Some social workers are technically employed by a staffing firm that contracts with a county CPS office. Unless the staffing firm itself is a qualifying nonprofit or government entity, those months of employment do not count.3

- Nonprofit organizations with atypical structures: A small number of nonprofits might not hold 501(c)(3) status, for example certain chambers of commerce or professional associations. Verify tax-exempt status directly.

Verifying Your Employer's Eligibility

The safest course is to use the PSLF Help Tool at StudentAid.gov. The tool pulls data directly from the IRS and employer identification number database to confirm eligibility in real time. Social workers should:

- Complete the employment certification form annually or when changing jobs.

- Keep a personal record of all submitted forms and confirmation of qualifying payments.

- If an employer's status appears uncertain, contact the PSLF servicer (MOHELA) for written clarification.

- In the unlikely event that your nonprofit employer engages in illegal activity and loses PSLF eligibility in the future, payments made while the employer was in good standing still count toward the 120 required payments. The proposed rule contained this protection, and it is expected in any future attempt to tighten standards.4

Because rulemaking at the federal level can shift, monitoring Federal Student Aid announcements and organizations like the National Association of Social Workers can help you stay ahead of any changes that might affect your forgiveness timeline. Social workers pursuing licensure should also review social work licensure requirements by state, since employment setting and PSLF eligibility often intersect with licensure decisions.

PSLF Eligibility by Social Work Employer Type

Public Service Loan Forgiveness (PSLF) remains a critical pathway for social workers to eliminate remaining federal loan balances after 120 qualifying payments. The 2026 federal student loan policy changes do not directly alter PSLF employer eligibility criteria, but proposed borrowing caps and the potential elimination of graduate PLUS loans could affect how social workers finance their degrees before pursuing forgiveness. The table below clarifies which employer types qualify for PSLF under current rules, with no announced changes as of 2026.

| Employer Type | Example Settings | PSLF Eligible (Pre-2026) | PSLF Eligible (Post-2026) | Notes |

|---|---|---|---|---|

| Federal, state, or local government agency | Department of Social Services, VA, public schools | Yes | Yes | No change anticipated; government employment remains qualifying. |

| 501(c)(3) nonprofit organization | Community mental health centers, family service agencies | Yes | Yes | Must be full-time; many social work nonprofits qualify. |

| Non-501(c)(3) nonprofit that provides public service | Some non-profit hospitals or clinics not under 501(c)(3) | Yes, if primary purpose is public service | Yes, criteria unchanged | Eligibility depends on meeting the public service definition; verify with employer. |

| For-profit social service organization | For-profit behavioral health companies, private prison health care | No | No | For-profit employers generally do not qualify unless they contract with a government entity and meet specific employee-based criteria (rare). |

| Private clinical practice (self-employed) | Solo private practice or group practice owned by clinician | No | No | Self-employed social workers do not qualify for PSLF under current rules; independent contractor work does not count. |

| Indian tribal government or organization | Tribal social services, health clinics serving Native populations | Yes | Yes | Tribal government employment is qualifying; no changes. |

| Labor union or partisan political organization | Union of social workers, political campaign | No | No | Labor unions and political organizations are not qualifying employers unless they are 501(c)(3) and primarily provide a public service (unlikely). |

Loan Forgiveness and Repayment Programs for Social Workers

Two primary paths exist for social workers tackling student debt: Public Service Loan Forgiveness (PSLF) and targeted loan repayment programs like the National Health Service Corps (NHSC) Loan Repayment Program. The first wipes out remaining federal loans after a decade of qualifying payments; the second provides upfront lump sums in exchange for clinical service in underserved areas. Understanding how these programs intersect, and which state-level options you can layer on top, can dramatically reduce the financial weight of an MSW.

Public Service Loan Forgiveness (PSLF) for Social Workers

PSLF forgives the remaining balance on Direct Loans after you make 120 qualifying monthly payments while working full-time for an eligible employer. Most social work settings, including nonprofit agencies, public school districts, government health departments, and tribal organizations, count automatically. Payments must be made under an income-driven repayment (IDR) plan; as of 2026, options include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and the Saving on a Valuable Education (SAVE) plan. Because borrowers must recertify income and employer status annually, consistent documentation is essential. Social workers in roles ranging from child protective services to hospital discharge planning routinely qualify, but the program's administrative hurdles mean that many leave forgiveness on the table simply by failing to file the Employment Certification Form regularly.

National Health Service Corps Loan Repayment

The NHSC Loan Repayment Program targets licensed clinical social workers (LCSWs) who commit to at least two years of full-time clinical practice in a federally designated Health Professional Shortage Area (HPSA). Award amounts are tied to the HPSA score and the provider's specialty; social workers with LCSW credentials and a track record in mental health or substance use disorder treatment are prioritized. Typical awards range from $50,000 to $75,000 for the initial two-year contract, with the possibility of extending in one-year increments for additional funds. Because the NHSC payment is disbursed directly to loan servicers soon after you begin service, it can quickly reduce principal balances that would otherwise accumulate interest under IDR plans.

State-Level Loan Repayment Assistance Programs

Many states fund their own loan repayment incentives to draw social workers into schools, rural clinics, and behavioral health centers. State loan repayment assistance programs (LRAPs) are generally not social-work-specific; most cover behavioral and mental health providers, public service workers, or health professionals in shortage areas broadly.1 While details shift with each budget cycle, the following states have active programs that are especially relevant for MSW graduates:

- California: The Licensed Mental Health Services Provider Education Program awards vary based on the commitment length and site location, frequently reaching $50,000 for a multi-year service agreement in a public mental health setting.

- Washington: The Health Professional Loan Repayment Program offers up to $75,000 for two years of full-time clinical work in a shortage area, with a preference for providers serving Medicaid and uninsured patients.

- Texas: Through the Mental Health Loan Repayment Program, social workers providing therapy in underserved regions can receive up to $10,000 annually, often renewable for multiple years.

- Illinois: The Behavioral Health Workforce Loan Repayment Program provides up to $25,000 for a two-year commitment in a community mental health center or designated shortage area.

- New Jersey: The Tuition Reimbursement Program for mental health professionals offers $5,000 per year for up to four years to LCSWs working in state-approved facilities.

- Oregon: The Oregon Partnership State Loan Repayment Program is open to social workers in HPSAs and can match federal NHSC awards, effectively doubling the benefit for those who qualify for both.

California and Washington are consistently ranked among the most important states for social work employment, with large public and nonprofit sectors that align well with PSLF eligibility as well as state LRAP opportunities.2 Texas, meanwhile, has expanded its behavioral health infrastructure significantly, making state loan repayment options more accessible to MSW graduates entering large medical systems.3 Beyond these high-population states, Oregon is frequently cited among the top states for social workers in rural and underserved settings, where LRAP and NHSC awards can be combined for maximum impact.4

Stacking Repayment Strategies

A key advantage for social workers is that most federal and state programs are stackable, with careful planning. For example, you can accept an NHSC award while simultaneously making PSLF-qualifying payments if your NHSC service site is a nonprofit or government entity. The NHSC lump sum reduces your principal and interest, but the time you spend fulfilling the NHSC contract still counts toward the 120 PSLF payments. However, you cannot use a single year of service to satisfy the requirements of two repayment programs that both require a full-time service commitment. Some state LRAPs explicitly allow combination with federal PSLF, while others require you to choose one. Always verify written program policies before enrolling in multiple agreements. Prospective students exploring how to fund an MSW should also review MSW scholarships as an upstream strategy that reduces borrowed principal before repayment even begins.

IDR Forgiveness as a Backstop

For social workers who work in the private sector, part-time, or in non-qualifying settings, IDR forgiveness is the long-term safety net. After 20 or 25 years of payments under an IDR plan (depending on the plan and when you first borrowed), any remaining balance is forgiven. As of 2026, forgiven amounts under IDR plans are not treated as taxable income through at least 2025 under the American Rescue Plan provision; it is uncertain whether this exclusion will be extended. This backstop does not replace PSLF, since paying for two decades is far more expensive than ten, but it ensures that social workers with high debt relative to income will not carry loans into retirement.

Social workers often have the opportunity to stack Public Service Loan Forgiveness qualifying monthly payments alongside a National Health Service Corps lump-sum repayment award and a state's Loan Repayment Assistance Program. This triple benefit can dramatically reduce loan burdens, but careful tracking is essential: each program may target different loan types, and overlapping service commitments can create conflicts that risk disqualification.

Social Worker Salary Vs. Student Debt: What the Numbers Show

Social workers holding an MSW often carry student debt between $60,000 and $120,000, making salary a critical factor in loan repayment timelines. The table below shows salary distributions for social workers (all other categories) across select states, highlighting the wide gap between the highest- and lowest-paying regions. In top-paying Washington, the median annual salary of $96,550 provides more room for aggressive repayment, while in North Dakota, the median salary of $77,380 may stretch repayment periods even with income-driven plans.

| State | 25th Percentile | Median Annual Salary | 75th Percentile |

|---|---|---|---|

| Washington | $70,410 | $96,550 | $112,320 |

| Massachusetts | $72,880 | $94,000 | $112,650 |

| Georgia | $59,810 | $92,750 | $110,930 |

| South Carolina | $71,390 | $91,940 | $106,870 |

| Delaware | $63,400 | $91,710 | $106,580 |

| Mississippi | $52,770 | $89,860 | $98,550 |

| Texas | $53,200 | $89,520 | $113,840 |

| South Dakota | $77,000 | $89,320 | $96,870 |

| Alabama | $77,050 | $89,170 | $101,130 |

| Iowa | $72,550 | $88,000 | $100,820 |

| Virginia | $54,960 | $86,690 | $105,810 |

| Indiana | $62,150 | $80,410 | $94,310 |

| Minnesota | $65,810 | $79,220 | $92,800 |

| Maryland | $56,740 | $77,900 | $109,120 |

| North Dakota | $61,960 | $77,380 | $92,750 |

Social Worker Salary Distribution: National Overview

The 2028 earnings-test rule ties federal loan eligibility to whether graduates out-earn typical bachelor’s holders. Social work salaries often fall short of that threshold, putting program funding at risk for a workforce of 759,740.

MSW Borrowing Scenarios: Planning Your Finances Before and After 2026

Understanding how federal student loan changes affect your specific career path is essential for making informed financial decisions. The following scenarios illustrate common MSW trajectories, highlighting how new borrowing limits and repayment options play out in real terms.

Clinical Social Worker in a High-Cost Metro

- Debt: $65,000 in federal loans (pre-2025 graduate). Starting fall 2027, federal borrowing for the same program might cap at $40,000, requiring $25,000 in private loans to cover remaining costs.

- Income: $58,000 starting salary.

- Standard plan: $680 per month for 10 years.

- SAVE plan: $220 per month based on income; after 20 years (non-PSLF) any remaining balance is forgiven, though the forgiven amount may be taxed.

- PSLF: Monthly payments drop to $220, and after 10 years (120 qualifying payments) the remaining $52,000 is forgiven tax-free.

- Private loan impact: Private loans are ineligible for PSLF or IDR forgiveness. If the 2027 entrant relies on $25,000 in private debt, only the $40,000 federal portion benefits from forgiveness, leaving a much larger out-of-pocket burden.

School Social Worker in a Mid-Range State

- Debt: $45,000 in federal loans (pre-2025). Post-2026 caps might reduce eligible federal loans to $35,000, forcing $10,000 in private loans.

- Income: $50,000 starting salary.

- Standard plan: $480 per month for 10 years.

- SAVE plan: $180 per month; after 20 years, nearly $30,000 forgiven.

- PSLF: With 10 years in a qualifying school district, payments total about $21,600, and $35,000 is forgiven.

- Private loan reality: The $10,000 private loan must be repaid in full, typically at higher interest rates, adding $120 per month over 10 years and receiving no forgiveness.

Macro/Policy Social Worker

- Debt: $50,000 federal (pre-2025). New caps could slice this to $30,000, with $20,000 private.

- Income: $52,000.

- Standard plan: $530 per month.

- IDR plans: Around $200 per month, with forgiveness after 20 or 25 years (potentially taxable).

- PSLF: Only viable if the employer qualifies (e.g., a 501(c)(3) nonprofit). If so, payments and forgiveness mirror the SAVE estimate above.

- Private loan risk: Large private balances undermine the safety net of IDR forgiveness, making this path riskier under the new caps.

Borrowing Before and After 2026

A student who graduated in 2025 could access full Graduate PLUS loans, capping total debt by the cost of attendance minus other aid. Starting in fall 2027, the new earnings-test rule and phased-out Graduate PLUS limit federal borrowing to stricter program-specific caps. This could mean $20,000, $40,000 less in federal loans for a two-year MSW, shifting the gap to private loans.

Is an MSW Still Financially Viable?

An MSW makes strong financial sense if you commit to PSLF-eligible employment, attend an affordable program (especially online MSW program selection in-state public options), and minimize private borrowing. Before enrolling, review the average salary for social workers with a master's degree against your projected debt load. Consider alternative paths if your expected salary is far below the debt you must assume, your dream employer does not qualify for PSLF, or the program requires significant private loans that would outpace your repayment capacity. Always calculate total projected debt, including living expenses, and compare it to your realistic salary trajectory before enrolling.

What MSW Students and Social Workers Should Do Now

By 2028, U.S. Department of Education rules will require graduate programs to prove their graduates out-earn the typical bachelor's degree holder, a threshold many MSW programs may struggle to meet. Coupled with Grad PLUS loan elimination and new borrowing caps taking effect in 2026, the financial landscape for social work education is shifting quickly. Proactive steps now can protect your funding and career path.

Timeline: Key Policy Dates for MSW Borrowers

- 2026: Grad PLUS loans are eliminated for graduate students. New annual and aggregate federal loan caps reduce how much MSW students can borrow. PSLF employer eligibility rules tighten, potentially excluding some nonprofit and for-profit social work settings.

- 2028: The earnings-test rule begins. Graduate programs that fail to show graduates earn above the bachelor's-degree median in two out of three years lose access to federal Direct Loans and eventually Pell Grants.

For Current MSW Students

- Verify PSLF employer eligibility immediately. Use the Federal Student Aid PSLF Help Tool to confirm your current or intended employer qualifies under the 2026 updated criteria. If you are in a non-qualifying position, consider transitioning to an eligible setting before certification.

- Consolidate and certify employment now. Submit an Employment Certification Form annually to lock in qualifying payments under existing rules while the window remains open.

- Maximize federal borrowing before caps tighten. If you are eligible for Grad PLUS loans this year, assess whether additional borrowing for the 2026-2027 academic year can bridge the reduced limits in subsequent years. Talk to your financial aid office about transition rules.

For Prospective MSW Applicants

- Compare program costs aggressively. Use net price calculators to see true out-of-pocket costs for online vs. on-campus and public vs. private programs. Even small tuition differences compound under lower borrowing limits.

- Factor in the funding gap. With Grad PLUS eliminated, you may need to cover $10,000, $20,000 per year from savings, work, or private loans. Look for programs with employer-funded field placements, graduate assistantships, or tuition remission that minimize borrowing needs. Exploring MSW scholarships early can help close that gap before private debt becomes the default.

- Target programs with strong earnings outcomes. Ask admissions offices for recent graduate salary data and licensure exam pass rates. Programs likely to survive the 2028 earnings test have transparent, competitive outcomes.

For Working Social Workers

- Confirm your PSLF qualifying payment count. Log into your Federal Student Aid account and review your progress. If you are close to forgiveness, avoid actions that could reset the clock, like consolidating after July 2026.

- Stack NHSC and state loan repayment programs. The National Health Service Corps (NHSC) offers up to $50,000 in loan repayment for clinical social workers in underserved areas. Many states run parallel LRAPs that can be used on top of NHSC awards. Check the NHSC application portal for cycles and eligibility.

- Engage with advocacy organizations. The National Association of Social Workers (NASW) and the Council on Social Work Education (CSWE) are actively lobbying for earnings-test exemptions for essential professions. Join their advocacy alerts to support policy changes.

Tools and Resources

- Federal Student Aid PSLF Help Tool: Verify employer eligibility and generate forms.

- NHSC Loan Repayment Program portal: Apply for competitive service-obligation awards.

- NASW advocacy page: Track federal policy updates and participate in action campaigns.

Frequently Asked Questions About Social Work Student Loans in 2026

As the 2028 earnings-test policy approaches, MSW students and practicing social workers have pressing questions about loan eligibility, forgiveness, and career planning. Below are answers to the most common questions about federal student loans and social work in light of the new rules.