Points of interest…

- MSW students face a $20,500 loan cap while health professions get $50,000.

- CSWE continues advocacy after social work was excluded from federal loan expansion.

- Combining PSLF, NHSC, and state programs maximizes forgiveness for social workers.

Why doesn't social work qualify for the higher graduate federal loan limits that nursing and physician assistantship programs now receive? On July 1, 2026, the Department of Education expanded the list of professional degrees eligible for up to $50,000 in annual federal borrowing to 29 fields, but the master of social work was not included. MSW students remain capped at $20,500 per year, despite clinical social work requiring licensure equivalent to other health professions. This disparity leaves many graduate students unable to cover full tuition and living costs through federal loans alone, forcing riskier private borrowing. MSW scholarships can offset some of that gap, but advocacy organizations continue pressing for systemic inclusion, and the loan cap disparity remains a direct financial obstacle for the profession's pipeline.

What Changed on July 1, 2026: The Expanded Professional Degree List

On July 1, 2026, the Department of Education expanded the list of professional degree programs eligible for higher federal loan limits from 11 to 29 fields, but social work and education were left standing on the sidelines. The fight over which graduate programs count as 'professional degrees' reached a critical juncture that day, with immediate consequences for MSW students.

A legislative trigger meets a narrow interpretation

The One Big Beautiful Bill Act allowed the Education Department to designate professional degree programs for annual loan limits reaching $50,000, more than double the standard $20,500 cap for graduate students. But the department's first list, released in early 2026, included only 11 fields and excluded most licensed clinical professions. That narrow definition left out fields like advanced nursing and physician assistantship, which require extensive supervised clinical hours, a central characteristic of professional training.

Health-care fields sue and win a temporary expansion

Trade associations for advanced nursing and physician assistantship challenged the narrow definition in court, arguing that their programs' intensive clinical requirements met the department's own professional-degree criteria. D.C. District Court Judge Beryl Howell agreed, issuing a preliminary injunction that forced the department to expand eligibility to 29 programs on July 1, 2026.1 Under Secretary Nicholas Kent confirmed compliance but noted the department's intent to appeal the ruling.

Social work and education remain locked out

Despite the expanded list, MSW and education degrees were not added. The Council on Social Work Education called the omission a glaring oversight. "Without the addition of social work, the list of professional degree programs remains incomplete," CSWE's Matt Hooper told Inside Higher Ed.1 Social work students complete 900 to 1,200 hours of field education and must pass the ASWB licensing exam, yet they are left with the standard $20,500 loan cap. Meanwhile, peers in advanced nursing and physician assistant programs can borrow up to $50,000 annually. The gap leaves many MSW students relying on additional private loans or part-time work to cover the full cost of their education. CSWE and other advocates are now weighing further legislation or litigation to secure inclusion for social work.

Why Social Work Was Left Out, and What CSWE Is Doing About It

In November 2020, the CSWE submitted formal guidance to the Department of Education urging the inclusion of social work in the list of professional degree programs eligible for higher federal loan limits.1 That effort did not immediately succeed, but it set a foundation for ongoing engagement.

A Record of Advocacy

CSWE's 2020 submission argued that clinical social work requires a master's degree, supervised experience, and a rigorous licensing exam, mirroring the educational and professional rigor of other fields already on the list. Despite this, the department maintained a narrower definition until the July 2026 expansion, which added health-care disciplines following litigation but again excluded social work and education. CSWE's most recent advocacy updates, issued quarterly, show that the organization is actively monitoring the new $50,000 annual loan limit rule and related restructuring proposals, but it has not announced a public naming campaign or coalition letter on this specific issue.2

Current Strategy: Regulatory Engagement

CSWE's primary strategy relies on regulatory and legislative channels.1 Its RISE committee (Research, Innovation, and Social Work Education) is tracking federal loan restructuring, including the potential elimination of Grad PLUS loans and the creation of a new graduate loan type set to debut by July 2026.3 The committee is focused on implementation monitoring of these changes, suggesting that CSWE aims to shape the new loan landscape rather than fight only for inclusion on the existing professional degree list. No litigation has been filed by CSWE to challenge the exclusion, and the National Association of Social Workers (NASW) has not publicly documented recent actions on loan limits in its searchable archive.1 public policy fellowships for MSW students offer one parallel avenue for social workers to offset educational costs while engaging directly with the legislative process.

How to Stay Informed

For social workers following this issue, regular checks on CSWE's Advocacy and Policy page and the Department of Education's site for potential rulemaking or Federal Register notices are essential. Pending litigation can be monitored through PACER, though none is currently active.

CSWE's approach is one of quiet persistence, working behind the scenes to influence the regulatory architecture rather than launching a broad external campaign.

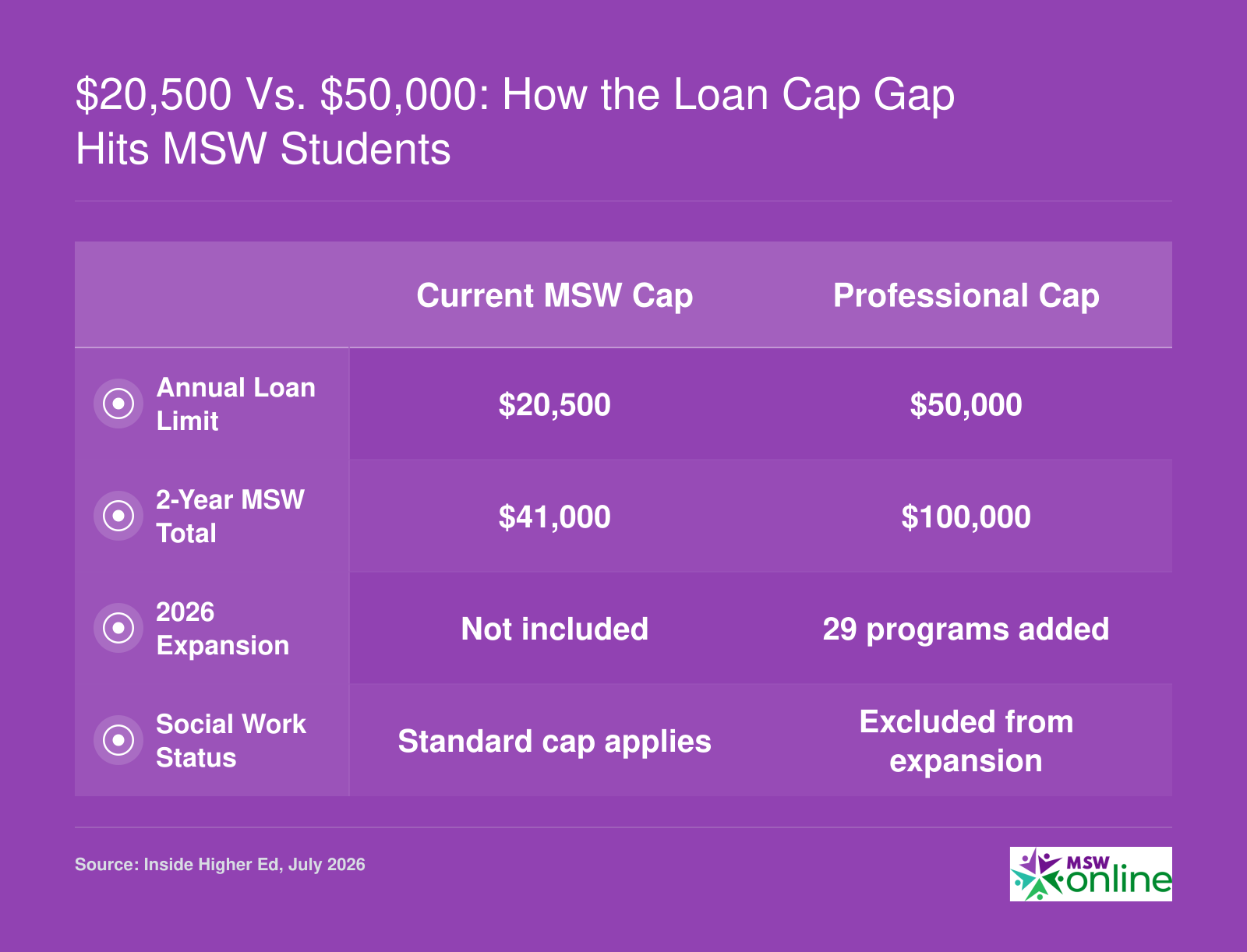

$20,500 Vs. $50,000: How the Loan Cap Gap Hits MSW Students

In July 2026, the Department of Education expanded higher loan limits to 29 professional degree programs, raising the cap to $50,000 annually. Yet social work, despite being a licensed clinical profession, was not included, leaving MSW students with the standard $20,500 limit and a significant funding shortfall.

Every Major Forgiveness Program Social Workers Can Use in 2026

Social workers can access at least four distinct loan forgiveness streams in 2026, but the rules for each program vary dramatically and a misstep can cost years of progress toward zeroing out your student debt.

Public Service Loan Forgiveness (PSLF): What the 2026 Rules Mean for Social Workers

PSLF remains the broadest path. Any clinical or nonclinical social worker can qualify if their employer is a government agency or a 501(c)(3) nonprofit. The final rule effective July 1, 2026, clarified employer eligibility under Executive Order 14235.1 The key change: organizations engaged in a "substantial illegal purpose" are now disqualified, but the Department of Education estimates fewer than 10 employers will be affected per year.3 Disqualification is prospective only, so any payments you made while the employer was still eligible still count toward your 120 qualifying payments.4 Affected employers have a 10-year reapplication window and can submit a corrective action plan to regain eligibility.1

For social workers at contract agencies, mixed-funding nonprofits, or privatized government services, nothing has fundamentally shifted. For-profit contractors generally remain ineligible, even if they do government work.5 If you work indirectly for a public entity through a staffing agency, make sure the actual employer on your W-2 is a qualifying government or 501(c)(3) organization. The rule was partially stayed by a court order,5 but the core 501(c)(3) and government employer definitions are unchanged. If you are already on track, your past payments are safe. If you are considering a new job, verify the employer's EIN and tax status through the PSLF Help Tool on Federal Student Aid.

NHSC Loan Repayment Program: Clinical Social Workers in High-Need Areas

The National Health Service Corps (NHSC) Loan Repayment Program targets fully licensed clinical social workers (LCSW or state equivalent) willing to practice in designated Health Professional Shortage Areas (HPSAs). Unlike PSLF, which forgives after 10 years, NHSC offers upfront lump sums in exchange for service. In 2026, licensed clinical social workers can receive up to $50,000 for a two-year full-time commitment, with options to extend for additional awards. Part-time awards are also available at half the full-time amount. The 2026 application cycle opened in early spring and closes in April, so interested social workers should plan a year ahead. To qualify, you must have a current, unrestricted clinical license and be working at an NHSC-approved site that is scoring high enough on a need-based scale. Because NHSC prioritizes clinical providers, nonclinical macro-social workers are not eligible even if they work in public health settings. For a deeper look at the MSW vs LCSW credential differences, that comparison can help you determine which license tier opens the most repayment doors.

State Behavioral Health Loan Repayment Programs

Many states run their own loan repayment initiatives for licensed behavioral health professionals, including clinical social workers. These often mirror the NHSC model but target state-specific shortage areas. Examples include New Jersey's Behavioral Health Loan Redemption Program (NJ BHLRP), New York's Licensed Social Worker Loan Forgiveness (NY LSWLF) program, California's Allied Healthcare Loan Repayment Program, and similar efforts in North Carolina and Michigan. Most require an LCSW or LMSW under clinical supervision and a commitment to work in underserved communities for two to four years. Award amounts and service obligations vary, and some states use a competitive scoring system. These programs can often be layered with federal options. Beyond loan repayment, social work grants for practitioners represent another funding layer worth exploring. The next section breaks down state-by-state details.

Income-Driven Repayment Forgiveness: A Taxable Backstop

If you do not qualify for PSLF or NHSC, or if you work in private practice or a for-profit setting, your final backstop is Income-Driven Repayment (IDR) forgiveness. Under current IDR plans, any remaining balance is forgiven after 20 or 25 years of qualifying monthly payments based on your income. However, a critical change took effect in 2026: IDR forgiveness is now federally taxable unless Congress extends the temporary tax exclusion that expired at the end of 2025. For a social worker with a six-figure loan balance after two decades of payments, this could mean a five-figure tax bill. Treat IDR forgiveness as your plan of last resort, and always calculate the potential tax liability before relying on it.

Social Work Loan Forgiveness Programs by State: A Comparative Overview

Unlike federal programs, state-level loan forgiveness for social workers is a patchwork of initiatives that changes annually, requiring graduates to actively monitor local options. In 2026, while many states offer repayment assistance, the criteria, award amounts, and eligible license types can differ dramatically, making a direct state-to-state comparison both necessary and challenging.

Start with Federal and National Directories

The Bureau of Labor Statistics provides broad occupational data but limited repayment specifics. Instead, visit the U.S. Department of Education's state contacts page or the Health Resources and Services Administration for links to state-level programs that may include social workers in health settings. These directories can point you toward agencies that administer behavioral health or primary care loan forgiveness, often overlapping with social work roles.

Navigate State Higher Education and Health Agency Websites

Each state's higher education agency or health department frequently manages loan forgiveness directly. For example, New Jersey's HESAA and New York's HESC have historically offered programs targeting mental health professionals, though eligibility shifts with budget allocations. Search for "[state] loan repayment social work" to locate official pages, and look for initiatives like Behavioral Health Loan Repayment or Rural Practice Incentives. Be prepared to review multiple agency sites, as programs may be housed under health, education, or workforce development divisions.

Leverage Professional Associations

NASW state chapters often compile lists of active repayment options, maintained by practitioners familiar with local legislation. These resources can highlight lesser-known social work grants for students or stipends not easily found through generic searches. Contact your chapter's advocacy or professional development coordinator for the most current information, as they track legislative changes and application windows.

Verify Details Annually

Because programs depend on state budgets and political priorities, always verify eligibility requirements, such as required licensure (LMSW vs LCSW degree and license differences), service commitment length, and award maximums, directly on official sites. Bookmark agency pages and check for updates each spring, when new funding cycles often begin. Treat any third-party list as a starting point, not a guarantee.

Can You Stack Programs? Combining PSLF, NHSC, and State Forgiveness

Yes, social workers can often combine multiple forgiveness programs to maximize debt relief, but careful coordination is required. Each program serves a different purpose, and they cannot be used to forgive the same dollar of debt twice. The general rule: PSLF forgives your remaining federal loan balance after 120 qualifying payments, NHSC Loan Repayment provides lump-sum awards that directly reduce your balance, and state programs add additional repayment assistance on top of that. The key is sequencing them so that each benefit arrives without disqualifying you from the next.

Understanding the Stacking Rule

These programs are complementary, not duplicative. PSLF is a forgiveness program, not a payment program; it wipes out whatever federal balance remains after a decade of public service. NHSC Loan Repayment, by contrast, is a grant that pays down a portion of your loans in exchange for service at an approved site. State programs vary but often function like NHSC, offering conditional funds that reduce principal. Because they address different parts of your debt over different time frames, you can use them together as long as you meet each program's eligibility requirements independently and do not claim double credit for the same employment period.

A Real-World Stacking Example

Consider an LCSW with $80,000 in federal student loans. They commit to a two-year, full-time NHSC Loan Repayment position and receive the maximum $50,000 applied directly to their loan balance, leaving $30,000. During those two years, they work at a site that also qualifies for PSLF and make monthly income-driven repayment (IDR) payments. Those 24 payments count toward PSLF. After the NHSC service ends, they continue at a PSLF-eligible employer for eight more years of IDR payments, and the remaining $30,000 plus any accrued interest is forgiven tax-free. If they also secured a state repayment award, those funds could further reduce the balance, potentially shortening the time needed to reach full PSLF forgiveness (though they cannot claim state funds and NHSC for the same service period). Loan forgiveness for rural social workers is one context where this kind of stacking is especially common, since many NHSC-approved sites are located in underserved rural areas.

Sequencing Your Benefits

To stack effectively, start NHSC first because it provides the largest immediate paydown. Ensure your employer qualifies for both NHSC and PSLF from day one. While serving the NHSC commitment, continue making your own monthly IDR payments; those are the only payments that count toward PSLF. After the NHSC term, you can stay at the same employer or move to another qualifying organization. If your state offers a repayment program, apply for it as soon as you are eligible, but check rules on concurrent service: some state programs allow you to serve their commitment simultaneously with PSLF, while others require a separate service period.

The PSLF Coordination Pitfall

A critical detail: NHSC lump-sum payments do not count as qualifying PSLF payments. Only the monthly payments you personally make under an IDR plan count toward the 120-payment requirement. If you mistakenly allow the NHSC payment to cover your upcoming monthly obligations, you may lose PSLF credit for those months. To avoid this, keep making your own payments each month even while the NHSC funds are being applied. You can request that the NHSC payment be applied to principal only, but servicer policies differ. The safest route is to maintain your own monthly payment schedule and accept that the NHSC money will simply reduce your overall balance.

Private Loans Remain Outside the Safety Net

None of these stacking strategies apply to private student loans. Federal forgiveness programs, NHSC, and state assistance are exclusively for federal loans. Social workers who had to borrow private loans because federal limits were too low will have to repay those in full, with no option to combine relief. This underscores the urgency of the push to raise graduate loan caps for MSW students: keeping all borrowing within the federal system is essential for stacking to work. In the meantime, MSW scholarships can help reduce upfront borrowing and keep more of your debt inside the federal system where these protections apply.

Tax Implications of Social Work Loan Forgiveness in 2026

A $40,000 forgiven balance under an income-driven repayment plan can generate a federal tax bill of approximately $8,000 to $10,000 in 2026, depending on the borrower's tax bracket, now that the American Rescue Plan Act's tax-free exclusion has expired. Understanding which forgiveness programs create tax liability and which do not is essential for social workers planning their repayment strategy.

PSLF Remains Tax-Free

Public Service Loan Forgiveness (PSLF) continues to be exempt from federal income tax.1 The full amount forgiven through PSLF is not considered taxable income, so borrowers working in qualifying public or nonprofit settings do not face a surprise bill after 120 qualifying payments.

IDR Forgiveness Is Now Taxable

Income-driven repayment (IDR) plans offer forgiveness after 20 or 25 years, but that forgiven balance is now fully taxed. The American Rescue Plan Act had temporarily excluded student loan forgiveness from federal income through the end of 2025,2 but with that provision expired, IDR borrowers who receive forgiveness in 2026 and beyond must report the forgiven amount as income. For a social worker with a $40,000 balance forgiven, this could add a significant four-figure tax liability in the year of forgiveness.

NHSC and State Program Variability

NHSC loan repayment awards are treated as taxable income and reported on a W-2, increasing a social worker's adjusted gross income for that year. State-based forgiveness programs vary widely.3 Some, like those in California, New York, and New Jersey, often exclude forgiven education debt from state taxable income even when it remains federally taxed. However, states such as Arkansas, Indiana, Mississippi, North Carolina, and Wisconsin do not offer such exclusions, meaning borrowers in those states may face both federal and state tax obligations on forgiven amounts.

Planning for Combined Tax Exposure

When stacking multiple forgiveness programs, the cumulative tax impact can be unpleasantly large. A social worker receiving both NHSC loan repayment and IDR forgiveness in the same year could face a compounded tax liability. For social workers also weighing broader financial planning for social workers, factoring in loan forgiveness tax exposure alongside retirement savings is equally important. Because legislative changes at both federal and state levels can shift tax treatment annually, consulting a tax professional who understands education-specific provisions is strongly recommended.

What Social Workers Earn Vs. What They Owe: The Debt-To-Income Reality

The federal graduate student loan cap for most programs remains at $20,500 per year, and social work master's degrees are not currently included in the higher $50,000 professional degree loan limit. For many MSW graduates, this means borrowing to cover tuition and living expenses while entering a field where national median salaries often start below $60,000. The table below highlights how earnings for core social work occupations stack up against the typical debt load.

| Occupation | Total Employment | Mean Annual Wage | 25th Percentile | Median Annual Wage | 75th Percentile |

|---|---|---|---|---|---|

| Child, Family, and School Social Workers | 382,960 | $62,920 | $47,480 | $58,570 | $74,060 |

| Healthcare Social Workers | 185,940 | $72,030 | $55,360 | $68,090 | $83,410 |

| Social Workers, All Other | 64,940 | $74,680 | $52,010 | $69,480 | $95,390 |

Frequently Asked Questions About Social Work Loan Forgiveness

Navigating loan forgiveness options can be confusing for social workers, especially with recent changes to federal loan limits and ongoing advocacy for MSW programs. Here are answers to common questions about maximizing debt relief in 2026.

Related Articles

Social work remains the only major licensed clinical profession still locked out of the $50,000 annual federal loan cap, despite serving communities with the same intensity as the health-care fields added in July 2026.

The $20,500 cap forces MSW students to borrow more from higher-interest private lenders or delay graduation. The Council on Social Work Education is actively pressing for inclusion, but achieving parity will require a louder collective voice. Readers can support that effort by joining CSWE and NASW advocacy campaigns and contacting their congressional representatives this fall. If you are still mapping your educational path, reviewing tips for incoming MSW students on financial aid and scholarships can help you minimize federal borrowing from the start. The most immediate step, however, is to calculate exactly how much forgiveness you could secure today. That audit is the first move toward a more affordable social work career.